What Is Financial Psychology? Understanding the Emotions Behind Financial Decisions

Many people understand money management principles fairly well, yet in practice they still overspend, avoid checking their bank accounts, or keep putting off saving.

The issue often does not lie entirely in knowledge or calculation skills, but in how emotions, beliefs, and habits influence daily financial decisions. That is exactly why it is important to understand what financial psychology is.

Once you recognize the psychological factors behind your spending, saving, and investing behaviors, it becomes much easier to adjust your personal finances in a more sustainable way.

Table of Contents

1. What Is Financial Psychology?

A simple definition of financial psychology

Financial psychology is the psychological side of how a person thinks, feels, reacts, and makes decisions about money. It includes emotions, beliefs, experiences, fears, biases, and habits related to spending, saving, debt, investing, and the sense of financial security.

Put simply, financial psychology explains why two people with the same income can still behave very differently with money. Because of their habits and underlying mindset, one person may plan ahead and stay disciplined, while another may spend emotionally, postpone saving, or avoid facing their financial situation directly.

- Emotions affect how you spend, hold, and respond to risk with money

- Money beliefs are often formed early and quietly shape financial behavior

- Past experiences can make financial decisions inconsistent, even when knowledge is not lacking

Why this is not just about “knowing personal finance”

Many people know they should save, avoid bad debt, and control spending, yet still struggle to do those things consistently. The gap between knowing and doing usually does not come down to formulas. It comes down to behavior, emotional self-regulation, and deep beliefs about money.

Money is also closely tied to anxiety, shame, self-reward, and status pressure, so financial decisions are rarely purely rational. That is also what makes financial psychology different from behavioral finance or investment psychology. It has a broader scope and is more closely connected to everyday personal finance.

2. Why Does Financial Psychology Strongly Affect Personal Life?

Money is not just numbers. It is also tied to a sense of security.

Money is not only used to pay for daily needs. It is also tied to security, freedom, and the ability to choose. It is directly connected to survival, family responsibility, future goals, and even a person’s sense of status, so people’s reactions to money are often more emotional than purely logical.

That is why financial psychology has a deep effect on how people hold money, spend money, and make long-term decisions. When a person’s sense of financial security is shaken, their financial behavior can become unstable, even if they understand the basics.

Many personal financial decisions happen in emotional states

In real life, many personal finance decisions are not made calmly or with full calculation. Many people spend to relieve stress, avoid checking statements when they feel pressured, or delay money plans because they are tired, anxious, or mentally overloaded.

- Spending to soothe emotions can throw off your budget

- Avoiding the real numbers often makes financial problems last longer

- FOMO around other people’s lifestyles can lead to poor-fit financial decisions

These reactions show that financial psychology is not a side issue. It directly affects daily money behavior. From there, the more important question becomes: what factors shaped that psychology in the first place?

3. The Main Factors That Shape Financial Psychology

Money experiences from family and childhood

A large part of financial psychology is formed very early through family environment and early experiences with money. Research on financial socialization shows that children gradually absorb habits, norms, attitudes, and money beliefs from parents, caregivers, and the environment around them.

Growing up in scarcity, debt pressure, or an overly restrictive spending environment can leave lasting marks. It is not just how a family uses money that matters. The way parents talk about money, worry about money, or avoid talking about money also helps shape financial behavior in adulthood.

Most people do not even realize that their thoughts about money are influencing their decisions. But those thoughts have a very large impact.

Underlying money beliefs

After childhood, many people develop “money scripts,” meaning underlying beliefs about money that may be unconscious but still strongly shape behavior. Recent financial education sources describe these beliefs as factors that can directly affect how a person spends, saves, invests, and manages financial life.

- Money is hard to hold on to

- Rich people are usually greedy

- Making money is very hard, so investing feels too risky

- If you have money, you should reward yourself right away

These beliefs are not always completely wrong, but they can distort financial decisions if they are not recognized in time.

Personality, risk tolerance, and response to uncertainty

Personality also shapes financial psychology in very different ways. Some people avoid risk too much, some make decisions too quickly, and some need complete control, which makes it hard for them to adapt when money plans change.

Living environment, social pressure, and social media

Besides family and personality, a person’s current environment also constantly affects daily financial behavior. Lifestyle comparison, pressure to succeed, and social media influence can push many people to spend more or set money goals beyond what their actual income can support.

Financial shocks and strong emotional memories

Experiences such as job loss, debt, failed investments, or family burdens often leave strong emotional reactions around money. After such experiences, some people become completely avoidant, while others control money too tightly to create a sense of safety.

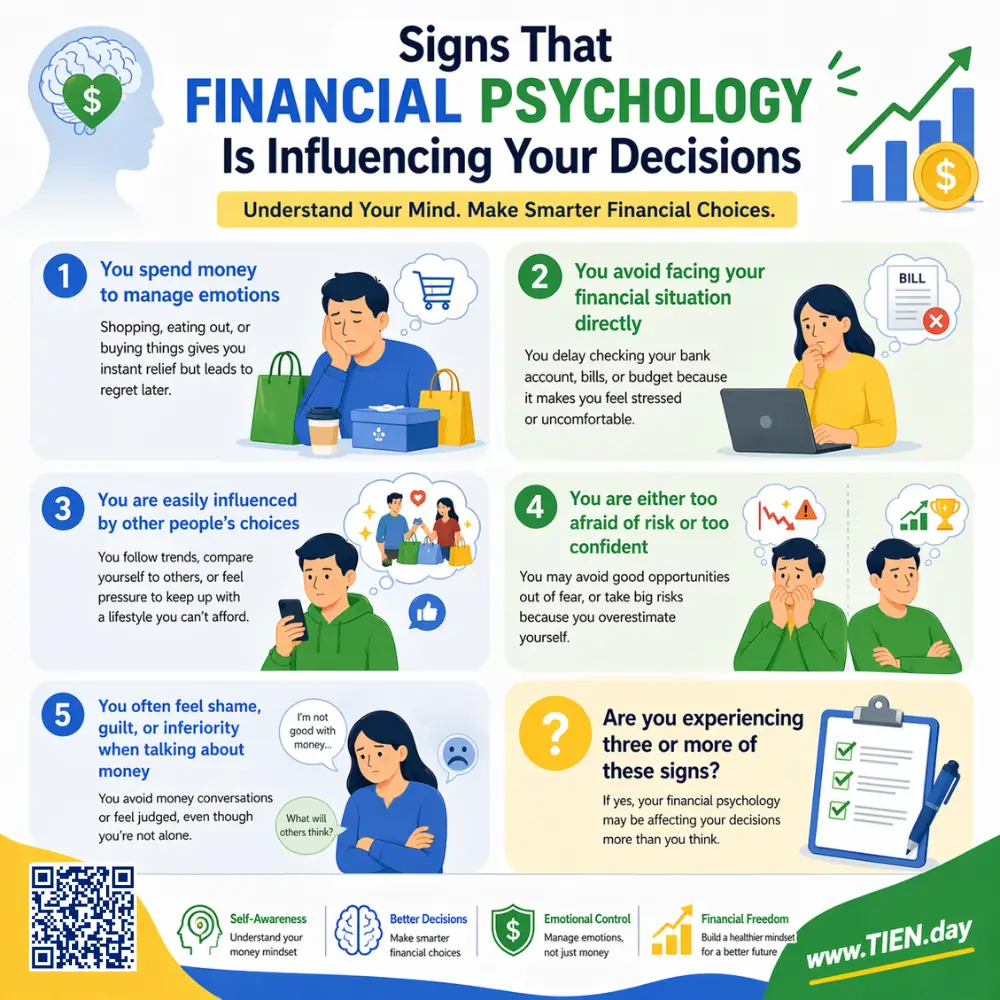

4. Signs That Financial Psychology Is Influencing Your Decisions

You spend money to manage emotions

One common sign of financial psychology at work is using spending as a way to regulate emotions during the day. When they feel sad, stressed, or have just achieved something small, many people quickly buy something as a reward, even if the expense is not truly necessary and shifts financial priorities.

You avoid facing your financial situation directly

Some people are not impulsive spenders, but they respond by avoiding money-related numbers. They hesitate to open banking apps, do not want to total up their debt, put off reviewing spending, and sometimes do not even know how much money they actually have left.

You are easily influenced by other people’s choices

When financial psychology is unstable, you are more likely to be pulled along by people around you. You see friends investing and want to follow, see others upgrading their lifestyle and start spending more, or see a new financial trend and want in immediately without properly judging whether it fits you.

You are either too afraid of risk or too confident

Two common extremes are holding on to money so tightly that you do not dare act at all, or committing money too quickly because you believe you are always in control of the outcome. Both reactions suggest that financial decisions are being driven more by emotion, bias, and personal risk tolerance than by a clear system.

You often feel shame, guilt, or inferiority when talking about money

Financial psychology can also show up through shame, self-blame, or embarrassment around money. These emotions cause many people to avoid discussing money with a partner or family, and to withdraw from managing their finances altogether.

Are you experiencing three or more of these signs?

If so, the issue may not be only about skill. It may also involve your behavior and beliefs about money.

- Early recognition makes it easier to fix your financial system

- It is better to notice the pattern before the problem drags on

5. Common Biases and Psychological Reactions in Financial Psychology

Fear of loss is often stronger than the desire for gain

A very common reaction in financial psychology is fearing loss more than wanting additional benefit. As a result, many people avoid change, avoid investing, or avoid restructuring their finances, even when their current approach is no longer effective, simply because it still feels familiar and safe.

Present bias: preferring immediate rewards

Another common pattern is choosing what feels good right now over a more distant future benefit. This makes it hard for many people to save for long-term goals, because the pleasure of buying now often feels stronger than the motivation to build gradually over time.

Mental accounting: seeing money through emotional categories

People do not always look at money as one unified whole within their personal cash flow. Many spend more freely when it comes to bonuses, unexpected income, or money outside the normal plan, while tightly controlling their fixed monthly salary.

- Bonuses are often seen as “easier to spend” than salary

- Unexpected income is more likely to be spent impulsively

- This compartmentalized view reduces overall financial control

Herd behavior and financial FOMO

Financial psychology is also strongly affected by the surrounding environment, especially when other people constantly display success or attractive lifestyles. In those situations, many people follow the crowd, invest based on hype, or increase spending just so they do not feel left behind.

Overconfidence or excessive avoidance

Some people overestimate how much control they have over their finances, so they commit money too quickly and too confidently. Others are so afraid of making mistakes that they do not act at all, hold money too tightly, and miss necessary opportunities to adjust.

Looking more broadly, these reactions show that financial psychology does not operate with perfect logic the way many people assume. Once you realize you are leaning toward loss aversion, immediate rewards, or crowd pressure, it becomes easier to adjust your money behavior in a calmer and more sustainable direction.

6. How Is Financial Psychology Different from Money Psychology, Behavioral Finance, and Investment Psychology?

Financial psychology and money psychology

Financial psychology and money psychology are very close concepts, so in practice they often overlap. Still, money psychology tends to focus more on beliefs, emotions, and a person’s relationship with money, while financial psychology is broader because it also covers behavior, decision-making, and how a person manages everyday financial life.

Financial psychology and behavioral finance

Behavioral finance mainly provides a framework for explaining biases, cognitive distortions, and patterns of decision-making that are not fully rational. Financial psychology goes closer to the individual person, including life experience, emotions, family background, and underlying beliefs formed over time.

- Behavioral finance helps name common biases

- Financial psychology helps explain why different people react differently to the same money issue

Financial psychology and investment psychology

Investment psychology is a narrower branch focused on decisions in investing, markets, and asset risk. Because of that, this page should stay centered on personal finance in general rather than shifting too heavily into investor behavior, market FOMO, or reactions to price swings.

Overall, financial psychology is the broadest concept among these three closely related ideas in the context of personal life. Making that distinction clear from the start helps readers choose the right content for their needs.

7. How to Improve Financial Psychology in a Healthier Direction

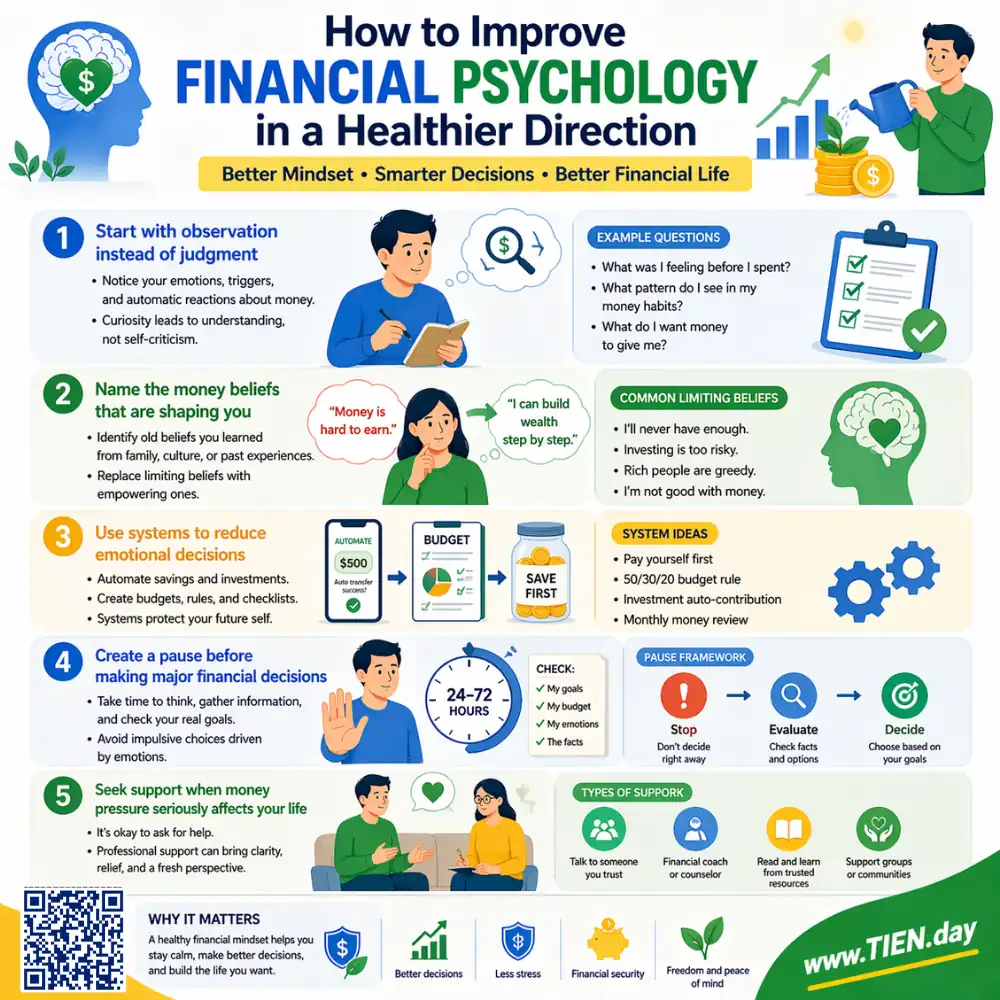

Start with observation instead of judgment

The first step in improving financial psychology is to observe your money behavior honestly instead of blaming yourself too quickly. Notice when you spend emotionally, avoid checking your accounts, or make decisions when you are tired. This helps you recognize repeated behavior patterns underneath the surface.

Name the money beliefs that are shaping you

After recognizing the behavior, write down the thoughts you often have about money. When you clearly see beliefs such as “making money is very hard” or “if I have money, I should reward myself right away,” it becomes easier to separate reality from old psychological reflexes that are pulling your behavior off track.

If you believe success is out of reach, you will never try. But if you believe you can learn and grow, you will begin to take meaningful action.

Use systems to reduce emotional decisions

One of the most practical ways to stabilize financial psychology is to reduce how often you have to make money decisions based on impulse. With a simple system in place, you are less likely to be pulled around by temporary emotions and more likely to stay disciplined in daily personal finance.

- Automatically transfer savings right after payday

- Use a simple budget that is clear enough to follow each month

- Review your money weekly or monthly to fix problems early

- Separate funds clearly so you do not mix spending and act impulsively

These tools do not remove emotion completely, but they help financial behavior become more stable over time.

Create a pause before making major financial decisions

When you feel overly anxious or overly excited, avoid making big financial decisions immediately. A 24-hour waiting rule for large purchases, or a short checklist before an investment decision, is often enough to reduce mistakes caused by temporary emotion.

Seek support when money pressure is seriously affecting your life

If financial stress continues for a long time, or avoiding money has become a repeated pattern, do not dismiss it. In those cases, support from the right professional can help address both the behavior and the emotional pressure connected to money.

8. How Does Financial Psychology Relate to Other Personal Finance Topics?

Its connection to personal financial management

Financial psychology directly affects whether you can stick to a stable money management system. Even when you already have a clear budget or plan, your emotions and beliefs about money still determine whether you can stay consistent, make timely adjustments, and feel in control of your daily finances.

See more Personal Finance Management: A Path to Financial Freedom

Its connection to financial habits

Many financial habits are actually repeated expressions of deeper money psychology and beliefs. When you regularly spend to reward yourself, avoid checking your accounts, or postpone monthly reviews, the issue is not only about skill. It also reflects behavior patterns that have been reinforced over time.

Its connection to saving and emergency funds

Difficulty saving is often not just a math problem. It is a conflict between present emotions and future goals. That also explains why many people understand the value of an emergency fund but still delay starting or withdraw money too early. See more Saving money: Easy ways to start and maintain effectiveness.

Its connection to personal cash flow and financial goals

When financial psychology is unstable, personal cash flow and financial goals are easily disrupted by short-term decisions. That is why understanding the psychology behind money behavior helps you stay aligned with long-term direction across your whole personal finance system.

Frequently Asked Questions About Financial Psychology

-

Is financial psychology only related to investing?

No. Financial psychology also affects spending, saving, debt, planning, and your everyday sense of financial security. Investing is only one narrower area where emotional reactions and biases may become more obvious.

-

Do low-income earners need to care about financial psychology?

Yes. People with lower incomes especially need to understand their emotional reactions to money so they can avoid emotional spending, avoid postponing planning, and avoid making decisions under pressure. Financial psychology is not only for wealthy people or large investors.

-

Are money psychology and money mindset the same thing?

They are close, but not exactly the same. Money mindset usually focuses more on the way you think about money and the perspective you hold, while money psychology is broader and includes emotions, underlying beliefs, and behavioral reactions.

-

Is learning financial knowledge alone enough?

Not yet. Knowledge helps you understand what you should do, but financial psychology affects whether you can keep doing the right things when you face stress, shopping temptation, or pressure from the environment around you.

-

When should you read more about investment psychology or behavioral finance?

You should go deeper into those topics once you already understand the foundation of personal financial psychology and want to explore decision-making biases or investment behavior in more detail. Those topics are better for deeper study, not as the main focus of this page.

Conclusion

Personal finance is not just about income, spending, or the numbers on a planning sheet. More importantly, it is also about how each person feels, reacts, and makes decisions about money in real-life situations.

When you truly understand financial psychology, it becomes easier to see the reasons behind repeated behaviors and start adjusting them in a more stable and sustainable direction.

To go deeper, you can continue with related topics such as money psychology, financial habits, personal financial management, or investment psychology to broaden your view and strengthen your overall personal finance system.

References:

- CFPB – Explore financial well-being findings

- CFPB – Pathways to financial well-being: The role of financial capability

- Creighton University – Creighton News

- CUNY Pressbooks – FinLit for Life: Teaching Financial Literacy at a Community College

- American Psychological Association (APA)- Face the numbers: Moving beyond financial denial

- APA – Speaking of Psychology

- Harvard Kenmedy School – Financial shame spirals