Personal financial planning: How to create a clear and easy-to-implement plan

Financial planning helps you understand why you still run short of money at the end of the month even when you have a salary.

The reasons often include emotional spending, unclear goals, and not tracking your cash flow.

In reality, financial planning is not just about writing things down. It is about managing money effectively. You need to set goals, then allocate your money for spending, saving, and investing.

That way, you can prioritize essential needs before short-term wants. This is the foundation for building an emergency fund, reducing financial stress, and creating sustainable savings. Starting personal financial planning early helps you stay in better control of your future.

1. What is personal financial planning?

1.1. The concept of personal financial planning

Personal financial planning is the process of setting financial goals and creating a practical strategy for using money wisely. It goes beyond basic expense tracking. It is a proactive way to manage your income, savings, investments, and financial decisions.

At its core, a personal financial plan helps you answer a few simple but important questions. How much money do you have? Where does it need to go? What should you prioritize first? Once those answers are clear, managing money becomes more purposeful and less reactive.

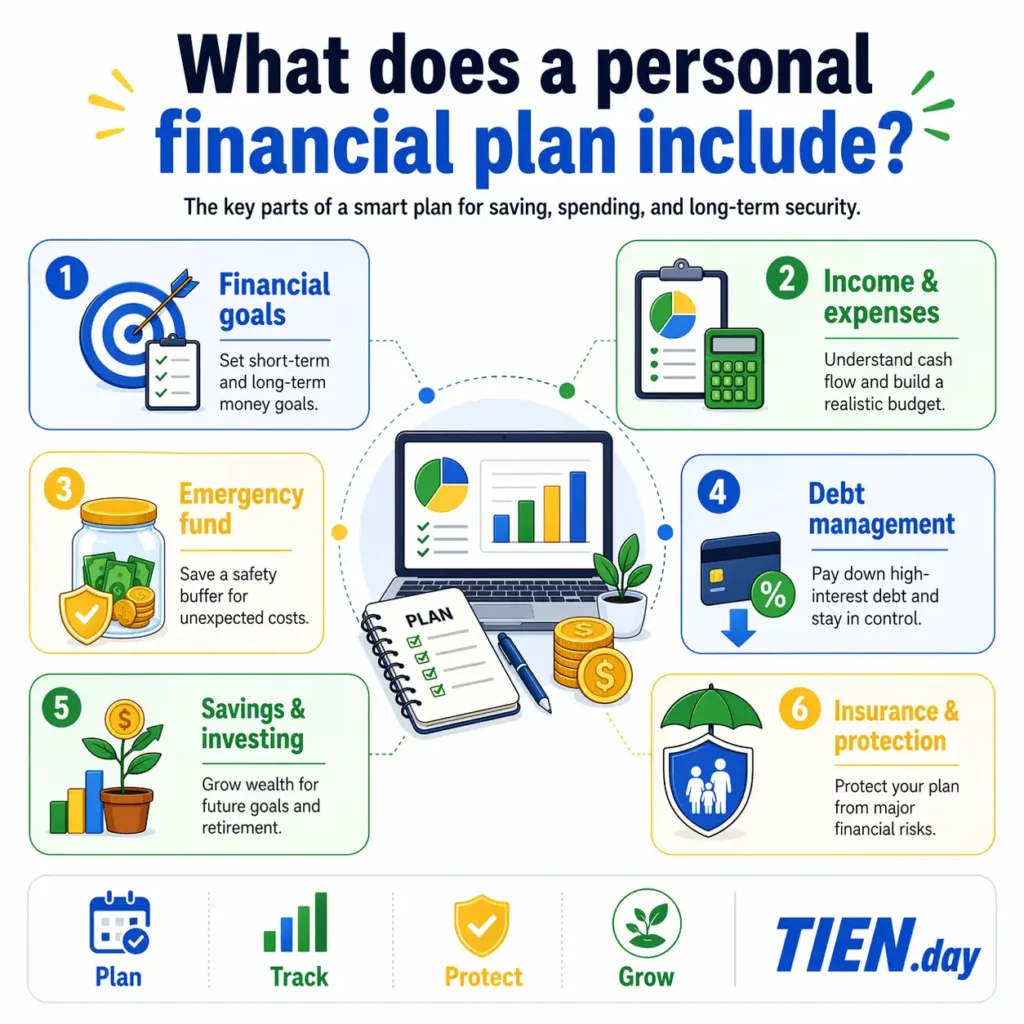

1.2. What does a personal financial plan include?

A personal financial plan usually includes these basic parts:

- Short-term, mid-term, and long-term financial goals

- Income from salary, business, or other sources

- Essential and flexible monthly expenses

- Savings for specific future goals

- Investments to grow your assets over time

- An emergency fund for risks or unexpected situations

- Ongoing tracking and adjustments to keep the plan relevant

1.3. Why should everyone start financial planning early?

Starting early gives you more time to build healthy money habits and improve your financial stability. A clear plan can reduce money stress, help you avoid emotional spending, and support major future goals such as buying a home, paying off debt, or preparing for retirement.

2. Why is financial planning important in personal finance management?

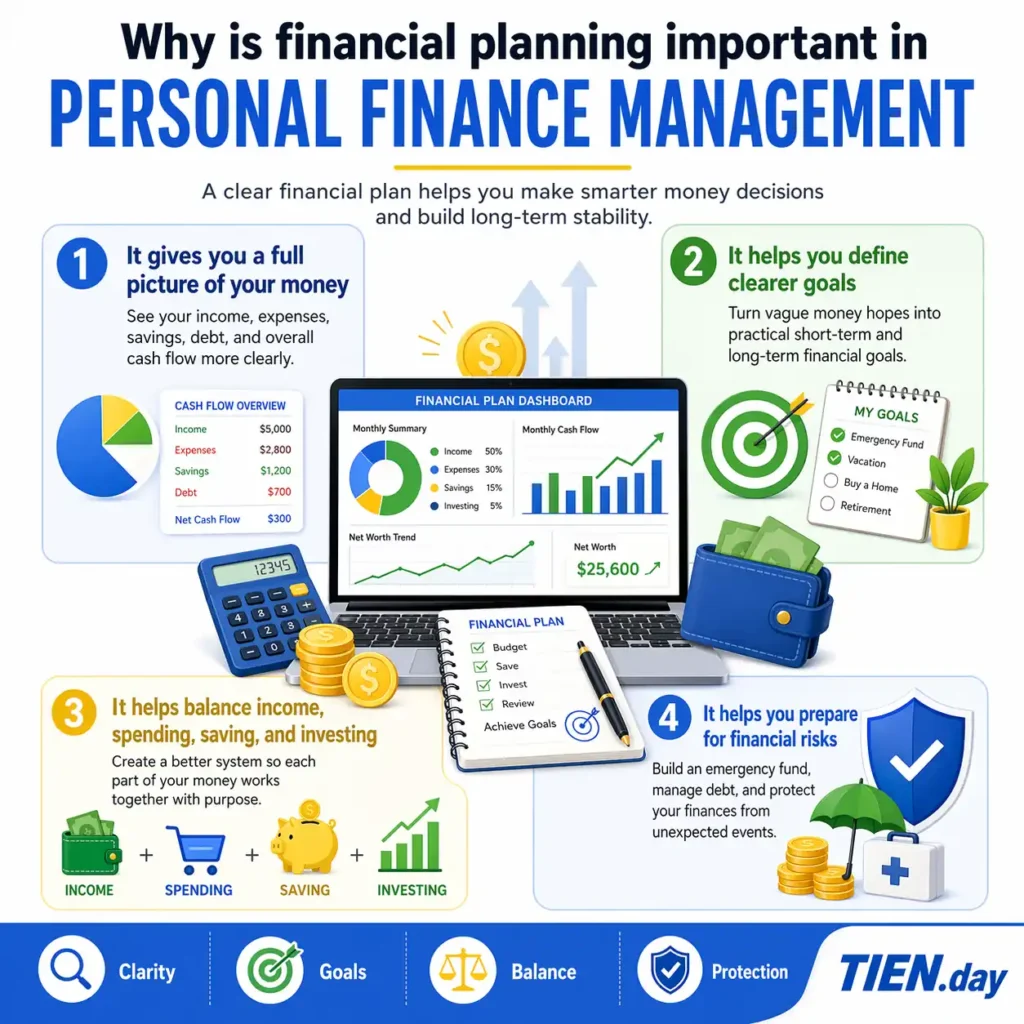

2.1. It gives you a full picture of your money

Financial planning helps you see the full picture of the money coming in and going out each month. This helps you better understand your current financial situation and your family’s finances.

You will know which expenses should come first and which ones can be reduced so your money is used more effectively. This is an important foundation for proactive and sustainable personal finance management.

2.2. It helps you define clearer goals

When you create a financial plan, it becomes easier to define both short-term and long-term goals. Clear goals help you know whether to save, invest, or pay off debt first.

Instead of using money based on emotion, you can allocate it intentionally according to your goals. This makes your personal financial plan more realistic and easier to stick with over time.

2.3. It helps balance income, spending, saving, and investing

Financial planning helps balance your income, spending, saving, and investing so you can avoid running short. You will know how much to keep for essential needs and how much to set aside for the future.

2.4. It helps you prepare for financial risks

A good financial plan also helps you prepare for unexpected risks in life.

- An emergency fund helps cover surprise expenses without disrupting your current budget.

- Insurance helps reduce the financial burden if you face health problems or an accident.

- Managing bad debt helps you avoid interest pressure and cash flow problems.

3. Seven effective steps to create a personal financial plan

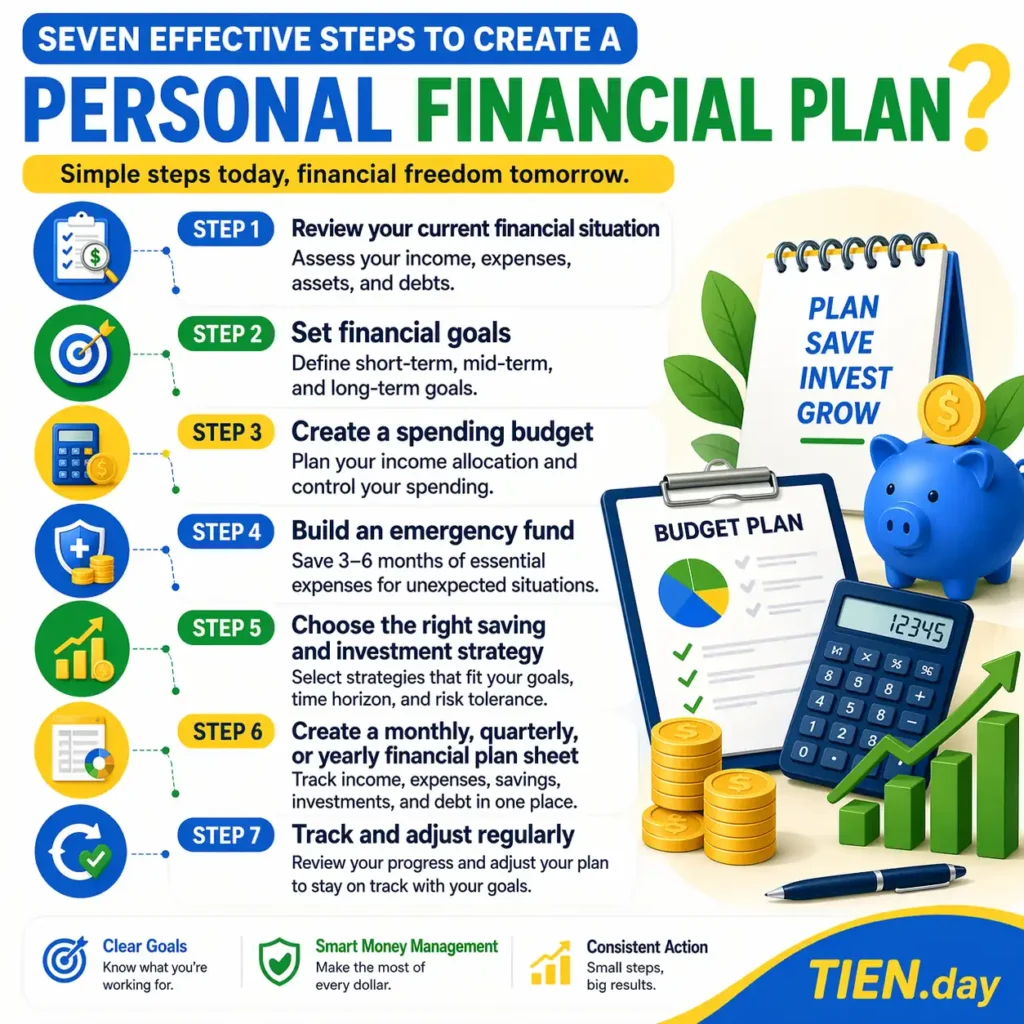

Step 1: Review your current financial situation

The first step in financial planning is to review your current financial situation. This helps you understand what you have, what you are missing, and where things are out of balance.

Start by listing all your income sources and financial obligations. When you can clearly see your current situation, it becomes easier to make better decisions.

- Income from salary, bonuses, business, or side income during the month

- Current assets such as cash, savings, gold, vehicles, property, or investments

- Debts such as personal loans, credit card debt, or consumer loans

- Fixed expenses such as rent, utilities, tuition, insurance, or installment payments

- Variable expenses such as food, transportation, shopping, entertainment, and unexpected costs

Step 2: Set financial goals

Once you understand your current situation, the second step is to set specific and realistic financial goals. Clear goals help you know how much you need to save and how long it may take.

To make those goals achievable, divide them into stages. This makes your personal financial plan easier to track and less stressful.

- Short term: buy a phone, pay off a small debt, build an emergency fund, or travel this year

- Mid term: buy a vehicle, learn new skills, or save business capital within two to five years

- Long term: buy a home, raise children, retire, or build lasting wealth over time

Each goal should have a specific amount, a deadline, and a clear priority level. This makes your financial plan more realistic and easier to carry out each month.

Step 3: Create a spending budget

The third step in financial planning is creating a budget that matches your income. This helps you control your money before it gets spent emotionally.

You can use simple methods to divide your money clearly and make the system easy to maintain. Two common methods are the 50/30/20 rule and the 6 jars method.

- 50/30/20: 50% for essential needs, 30% for wants, and 20% for savings

- 6 jars method: Divide money into essential needs, long-term savings, education, enjoyment, giving, and financial freedom

The important thing is to choose a method that fits your income, habits, and current goals. A good budget does not need to be complicated, but it does need to be clear enough for you to follow consistently.

Step 4: Build an emergency fund

An emergency fund is a safety cushion that helps keep you from falling into a financial crisis when something unexpected happens. A common target is three to six months of essential household expenses.

If your income is still low, you should still start with a small amount saved consistently each month. Saving little by little helps the fund grow without creating too much pressure.

You can keep this money in a separate account that is easy to access but not too easy to spend. Separating it this way helps protect your emergency fund from impulse purchases.

Step 5: Choose the right saving and investment strategy

Once you have a budget and an emergency fund, the next step is choosing the right saving and investing direction. Every investment decision should be based on your goals, time horizon, and risk tolerance.

If you want a high level of safety, you may prioritize savings accounts or suitable cash value insurance products. If you want better growth, consider learning about mutual funds or stocks through a plan that fits you.

- Savings accounts are suitable for short-term goals and preserving capital with relatively stable risk

- Mutual funds are suitable for people who want to invest regularly and have little time to watch the market

- Stocks are suitable if you can accept volatility and want to take advantage of investment opportunities

- Cash value insurance may be suitable if you want both protection and long-term accumulation

Step 6: Create a monthly, quarterly, or yearly financial plan sheet

After setting goals and deciding how to allocate your money, you should create a clear financial planning sheet. Understanding what a personal financial plan sheet is can help you manage your money in a more structured way.

This sheet can be organized by month, quarter, or year to track progress toward your goals. You only need to record income, expenses, savings, investments, debt, and your ending balance.

You can use Excel, Google Sheets, or even a notebook, as long as it is easy to update regularly. A simple and consistent system is more effective than a beautiful one you stop using halfway through.

Step 7: Track and adjust regularly

Financial planning only works when you track and adjust it regularly and seriously. Life is always changing, so your plan needs to stay flexible enough to reflect reality.

You should review your budget after one month to spot expenses that were higher or lower than expected. After three and six months, review your goals, savings rate, and investment performance.

If your income increases or your expenses change, you need to update your plan right away. The habit of tracking and adjusting consistently helps keep your financial plan sustainable and realistic.

Financial planning and savings essentials – Personal financial planning

4. How to build a personal financial plan for specific goals

4.1. Financial planning for buying a home

When planning financially for a home purchase, you need to define your target amount clearly. Then calculate the down payment, loan costs, and a realistic timeline for saving.

4.2. Financial planning for building an emergency fund

If you want more protection against risks, you should make a plan to build an emergency fund. A reasonable target is usually three to six months of essential monthly expenses.

- Set money aside as soon as you receive income

- Put it in a separate account to avoid emotional spending

4.3. Financial planning for paying off debt

If your goal is to pay off debt, you need to clearly record your total debt, interest rates, and payment deadlines for each loan. This helps you know which debt to focus on first to reduce financial pressure.

You should cut back on flexible spending and set aside a fixed amount each month for debt repayment. When you pay off bad debt early, your personal financial plan becomes more stable.

4.4. Financial planning for retirement

Retirement planning should start early because it is an important long-term goal. You should estimate the lifestyle you want and how much money you will need in the future.

- Save and invest consistently over the long term

- Review your plan regularly and adjust it when your income changes

5. Common methods for building a personal financial plan

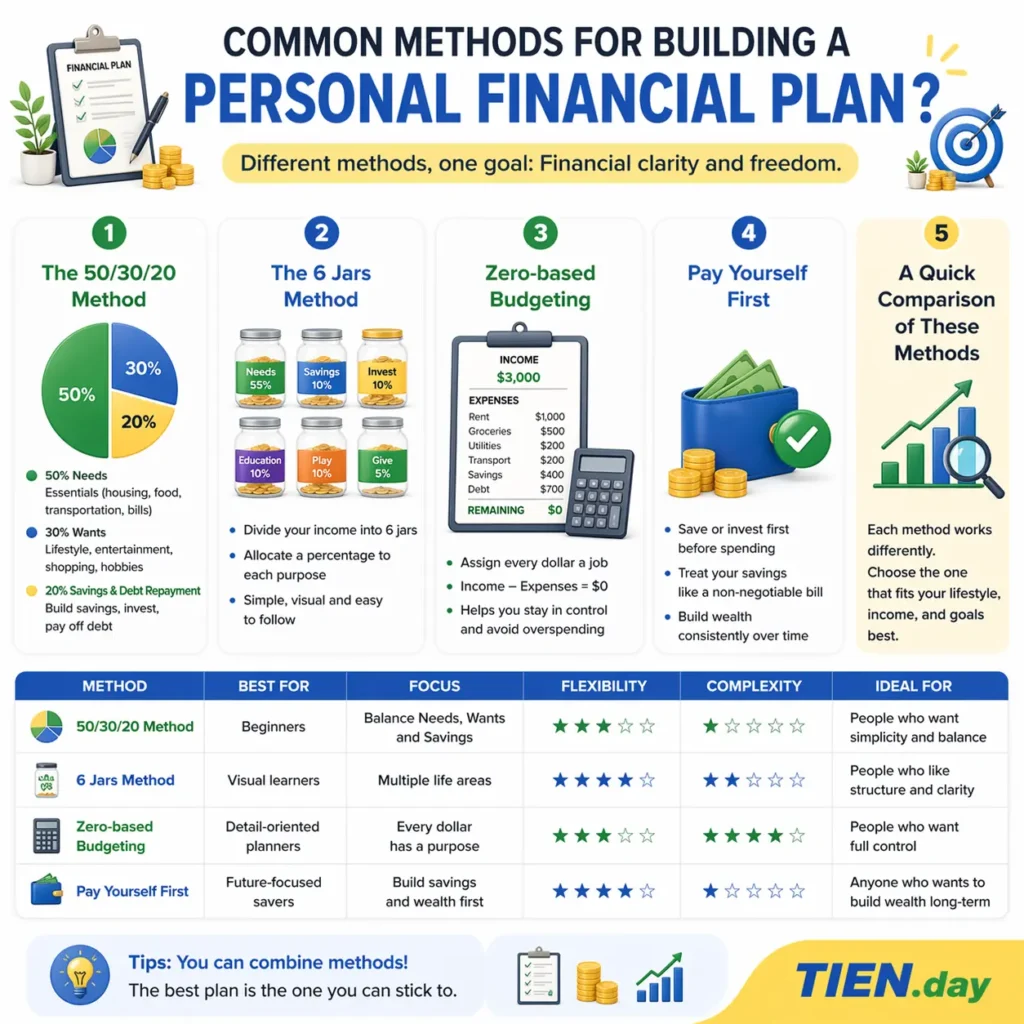

5.1. The 50/30/20 method

The 50/30/20 method is a simple financial planning approach that is easy for beginners to use. You divide your income into three parts: essential needs, personal wants, and savings.

- 50% for necessary costs such as housing, utilities, transportation, and tuition

- 30% for flexible spending such as entertainment, shopping, and personal experiences

- 20% for savings, investing, or debt repayment to improve your financial situation

5.2. The 6 jars method

The 6 jars method works well for people who want to divide their money clearly by purpose. This makes a financial plan easier to follow and helps control spending behavior.

- Essential needs

- Long-term savings

- Education

- Enjoyment

- Giving

- Financial freedom

5.3. Zero-based budgeting

Zero-based budgeting is a method where you assign your entire income to specific categories at the beginning of the month. Every dollar has a job, so it helps reduce emotional spending.

5.4. Pay yourself first

Pay yourself first means putting money into savings as soon as you receive income each month. This works well for people who want to build an emergency fund or grow savings steadily.

5.5. A quick comparison of these methods

If you want something simple, the 50/30/20 method is a good way to start financial planning quickly. If you prefer more detailed allocation, the 6 jars method and zero-based budgeting may be a better fit.

Pay yourself first is especially effective when your main goal is long-term saving and investing. Most importantly, choose a method that matches your income and real-life habits.

6. A simple personal financial planning template

6.1. What columns should a financial planning sheet include?

A personal financial planning template should be clear, easy to follow, and easy to update. The simpler the sheet, the easier it is to manage your monthly cash flow.

- Income from salary, bonuses, or other sources

- Essential expenses such as housing, utilities, and transportation

- Flexible spending for shopping and entertainment

- Savings for future goals

- Investments to grow your assets

- Debt and recurring payment obligations

- Emergency fund for unexpected risks

6.2. Should you use Excel, Google Sheets, or an app?

If you want flexibility, you can use Excel or Google Sheets to customize your planning sheet. This is a good place to add an internal link to an article about financial planning templates in Excel.

Expense tracking apps are good for people who prefer quick daily use on their phones. However, spreadsheets are still better when you need to track a detailed financial plan.

6.3. When should you choose a simple template, and when do you need a detailed one?

A simple template is suitable for beginners or people with only a few income and expense categories. A detailed sheet is better for families or people with multiple income sources.

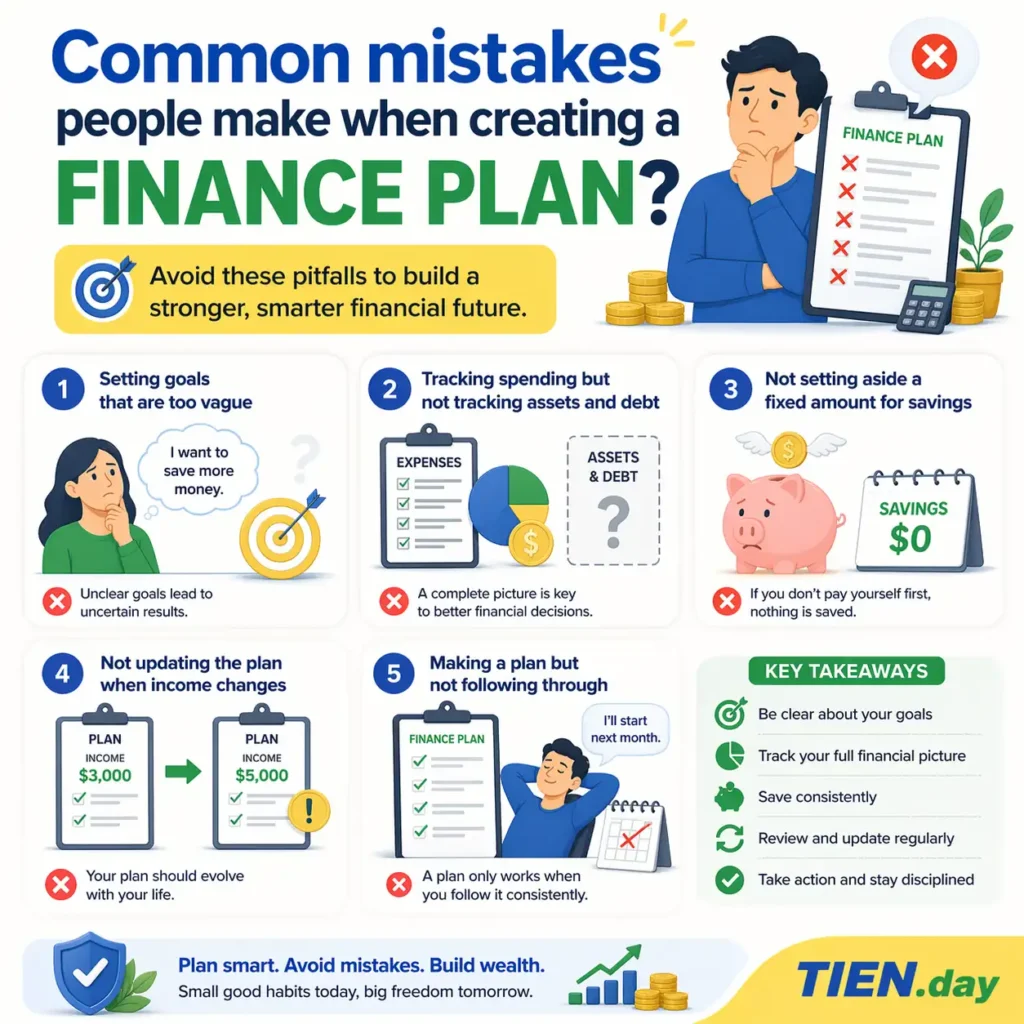

7. Common mistakes people make when creating a financial plan

7.1. Setting goals that are too vague

A common mistake in financial planning is setting goals that are too general and unclear. When goals are vague, it becomes hard to define the amount, the timeline, and the priority.

7.2. Tracking spending but not tracking assets and debt

Many people only record monthly expenses and ignore assets and debt. This makes the financial plan incomplete and gives an inaccurate picture of real financial health.

7.3. Not setting aside a fixed amount for savings

If you do not separate a fixed amount for savings in advance, it is very easy to spend all your income. Effective financial planning always treats saving as a required monthly category.

7.4. Not updating the plan when income changes

When income rises or falls, your financial plan should be adjusted accordingly. If you keep the old allocation, it becomes easier to lose balance between spending, saving, and investing.

7.5. Making a plan but not following through

Many people create a very detailed financial plan but do not stick to it in real life. A good plan only has value when it is tracked, applied, and adjusted consistently.

8. Who should start financial planning right now?

Financial planning is not only for people with high income or a lot of assets. It is a necessary habit for anyone who wants better control over money.

- New workers should make a financial plan so they do not spend their whole paycheck right away

- Young families need to manage income, expenses, and shared future goals well

- People with low or unstable income need a clear plan to reduce financial stress

- People who want to buy a house or car need steady saving and better cash flow control

- People who want financial freedom need to start with a clear and disciplined financial plan

Frequently asked questions about financial planning

-

Where should financial planning begin?

You should start by recording your income, spending, debt, and current assets. Once you clearly understand your current situation, financial planning becomes easier, more realistic, and less emotional.

-

Do you still need financial planning if your income is low?

Yes. People with low income still need financial planning so they do not spend beyond what they can realistically afford. A clear plan helps you prioritize essential needs, save small amounts, and reduce money stress.

-

How often should you track your financial plan?

You should track your financial plan every month so you can catch budget problems early. In addition, you should review it again after three or six months to make adjustments when needed.

-

Should you prioritize saving or investing first?

In the beginning, you should prioritize saving and building an emergency fund before investing. Once your financial foundation is more stable, you can allocate more money to suitable investment channels.

-

Is Excel enough for financial planning?

Yes. Excel is fully capable of handling financial planning if you want a system that is clear and flexible. For beginners, a simple spreadsheet is often easier to manage than many complex apps.

-

How is a financial plan different from a spending plan?

A spending plan focuses mainly on how you use money in the short term each month. A financial plan covers broader areas such as goals, savings, investing, debt, and long-term direction.

Conclusion

Personal financial planning is one of the most important foundations of long-term financial stability. It helps you understand your money, set realistic goals, control spending, build savings, and make better decisions over time.

You do not need a perfect system to get started. Begin by reviewing your current financial situation, setting clear goals, and creating a budget that fits your life. From there, build your emergency fund, choose the right saving and investment approach, and track your progress regularly.

You should start by reviewing your current situation, setting goals, and creating a budget that fits your life. After that, keep tracking regularly so you can adjust your financial plan as life changes.

- Read more about what financial planning is to better understand its role and purpose

- Download a financial planning template in Excel to start tracking your cash flow more easily

- Read an article about personal spending plans to optimize your monthly expenses

Vietnamese: Lập kế hoạch tài chính cá nhân: Cách xây dựng rõ ràng, dễ áp dụng

Reference

Banking magazine – Personal financial management: The role of budgeting and saving money