What Is Financial Freedom? The Right Way to Understand It and a Practical Roadmap

Many people think financial freedom is only for the very wealthy, for those who can retire early, or for people who already have a large source of passive income.

But in reality, it is not a distant destination or a one-size-fits-all formula. It is a state in which you gradually gain more control over your money and over the life decisions you make.

This article will help you understand the concept correctly, reflect on where you are now, and identify practical steps to move closer to financial freedom.

1. What Is Financial Freedom?

Definition of financial freedom

Financial freedom is the state of having a strong enough financial foundation to sustain the life you want without being completely dependent on a salary. In other words, you can still choose to work, but the pressure to earn money no longer controls every important decision.

Financial freedom is not just about having a lot of money

At its core, financial freedom is not about reaching a huge number. It is about how much control you have over risk and spending. Someone with a high income may still not be financially free if they lack an emergency fund, clear goals, and assets that generate cash flow.

Why this topic gets so much attention in personal finance

This topic matters because more and more people want to reduce money stress and live according to their own values. As living costs rise and career instability becomes more common, the need to take control of personal finances becomes more urgent.

- People also want to understand how to build an emergency fund, save, and invest so they can move closer to long-term goals.

- Readers want to know where they are on the path toward financial self-sufficiency and what foundations they are still missing.

2. How Is Financial Freedom Different from Financial Independence?

What is financial independence?

Financial independence is the point where you can pay for your living expenses without relying on outside support. Even so, at this stage, most people still need to work regularly to maintain their current lifestyle.

What is financial freedom?

Financial freedom is when your assets, accumulated cash flow, or passive income are enough to support the lifestyle you want over the long term. The key point is not just having money, but having enough freedom to make choices about work, time, and major life decisions.

A quick comparison based on three factors: source of income, level of autonomy, and freedom of choice

| Factor | Financial Independence | Financial Freedom |

|---|---|---|

| Source of income | Mainly earned income from work | Supported by assets, investments, or cash flow |

| Level of autonomy | Able to support yourself | Less dependent on a monthly paycheck |

| Freedom of choice | Able to manage life on your own | Able to choose how to live, work, or rest more flexibly |

Put simply, many people are already self-supporting but have not yet reached full financial freedom. If you want to understand the difference more deeply, you can explore financial independence further.

3. Is Financial Freedom the Same as FIRE or Early Retirement?

What is FIRE?

FIRE stands for “Financial Independence, Retire Early.” It is usually understood as a strategy focused on high savings rates, long-term investing, and optimized spending in order to shorten the period of dependence on earned income. (Reference: Investopedia)

Financial freedom does not require early retirement

Financial freedom does not mean you must leave work as early as possible. The core idea is having more choice. That means you may continue working because you want to, not because money pressure leaves you no alternative.

Read more about FIRE

If you want to learn more about high savings rates, withdrawal rules, and different early retirement models, FIRE is a more specific branch to explore. In other words, FIRE is only one possible path toward greater financial autonomy, not the only definition of financial freedom.

4. Signs You Are Getting Closer to Financial Freedom

You are no longer living entirely paycheck to paycheck

One early sign of financial freedom is that you no longer have to wait for your salary to cover essential expenses. This shows that your personal cash flow is becoming less fragile and that you have some breathing room to handle short-term disruptions.

You have an emergency fund and your bad debt is under control

You are moving closer to financial freedom when high-interest debt becomes less of a burden and you have a clear financial safety buffer. A very important foundation at this stage is building an emergency fund strong enough to keep short-term crises from derailing your entire plan. (Reference: CFPB, Techcombank)

You have assets or cash flow that help cover expenses

Once you have savings, income-producing assets, or additional sources of income that cover part of your spending, your financial autonomy begins to increase. This may not mean full financial freedom yet, but it does show that you are no longer relying on a single income source.

You can choose work based on more than just money pressure

At a more advanced stage, you may be able to take a break, switch jobs, or learn new skills without immediately falling into financial instability. When money has less power over major life decisions, that is another sign you are getting closer to real financial freedom.

5. How Much Money Do You Need for Financial Freedom?

There is no one number that works for everyone

There is no fixed number that guarantees financial freedom for all people, because everyone’s lifestyle, responsibilities, and circumstances are different. The right target usually depends on your annual spending, desired lifestyle, the age at which you begin building wealth, and your ability to generate income from assets.

How to estimate your target based on living costs and desired lifestyle

The most practical way is to calculate your total annual living expenses, then add costs for healthcare, housing, children, and long-term goals. Only after that should you estimate how much in assets you would need to generate sustainable cash flow, rather than aiming at a vague cash target.

What are the 4% rule and the rule of 25?

The 4% rule is a way to estimate how much you may be able to withdraw each year from an investment portfolio, typically over a period of about 30 years. From that comes the rule of 25: multiply your annual living expenses by 25 to estimate a reference target for the assets you may need. It is a useful framework, but not an unchanging formula. You should understand its origins and limits before applying it to your own goals.

The limits of the 4% rule in Vietnam

One important point of caution is that this rule was built from U.S. market data and assumes a withdrawal period of around 30 years. In Vietnam, you should also account for inflation, actual returns after fees, longer-than-expected life expectancy, healthcare costs, housing, and periods of unstable income. More recent sources also emphasize that 4% is only a reference point, not a guaranteed safe rule in every market environment.

Quick examples based on three common spending levels

15 million VND per month → 180 million VND per year → about 4.5 billion VND under the rule of 25.

30 million VND per month → 360 million VND per year → about 9 billion VND under the rule of 25.

60 million VND per month → 720 million VND per year → about 18 billion VND under the rule of 25.

These figures are only rough reference points to help you picture the journey toward financial freedom. They are not a substitute for a plan tailored to your real-life situation.

6. The Stages on the Journey to Financial Freedom

Why there are different stage frameworks

When learning about financial freedom, you will see some frameworks divide it into 5 stages, while others use 7 or 8. That happens because each framework is built from a different perspective, such as financial autonomy, the ability to retire early, or the size of accumulated assets.

So the goal of these stages is not to create one absolute scale for everyone. Their real value lies in helping you assess where you are, identify what foundations you are missing, and see what step should come next.

TIEN.day’s practical 5-stage framework

To make the idea easier to apply in real-life personal finance, TIEN.day suggests a simple, practical 5-stage framework:

Clear cash flow: You know what money is coming in, what is going out, and where the main leaks are each month.

Emergency buffer in place: You have a safety cushion strong enough to handle short-term disruptions.

Able to save and invest: You are not just covering expenses; you are also creating a sustainable surplus.

Assets generating cash flow: Part of your spending is now supported by income-producing assets or passive income.

Freedom to make life choices with less money pressure: You can make major decisions without being driven as heavily by income pressure.

Seen this way, financial freedom is not something that suddenly appears overnight. It is a gradual increase in financial autonomy. Once you understand what stage you are in, you can make more realistic plans and avoid setting goals that are too far removed from your current situation.

7. A Practical Roadmap Toward Financial Freedom

Step 1: Understand your personal cash flow clearly

If you want to move toward financial freedom, you need to know exactly where your money comes from, where it goes, and which expenses are leaking money on a regular basis. Without seeing that clearly, many people confuse the feeling of having a “decent income” with the reality that spending is quietly eating away at their ability to build wealth.

At this first step, the goal is not to cut every expense. It is to identify the cash flows that have the biggest impact on your financial health. If you still do not have a clear view of what comes in, what goes out, and where the leaks are, start by getting control of your personal cash flow. (Reference: CFPB, Techcombank)

Step 2: Build an emergency fund before talking about financial freedom

Many people want to invest early to speed up the journey, but a safety buffer is the first real layer of protection against unexpected events. If you do not yet have enough reserve funds for periods of job loss, illness, or interrupted income, you may be forced to pull money out of your savings halfway through.

So before thinking too far ahead about income-producing assets, make building a strong safety buffer for your current life the priority. This step makes the path toward financial freedom less fragile and less likely to be pushed backward by short-term crises.

Step 3: Pay off high-interest debt and reduce money leaks

Many people earn a decent income but still struggle to move closer to financial freedom because of high-interest debt and ongoing spending leaks. Credit card debt, consumer loans, or uncontrolled installment payments often weaken your ability to save and create much more psychological pressure than the numbers alone suggest.

Alongside debt repayment, you should also review recurring expenses that bring little real value to your life. Once you reduce financing costs and small monthly leaks, the money left over has a better chance of turning into real accumulated wealth.

Step 4: Increase your savings rate in a way you can sustain

Saving effectively does not mean forcing yourself to live too narrowly for a long time and then giving up halfway through. A healthy savings rate is one you can maintain consistently for years, even when your job and living situation change.

The important thing is that the money you set aside should be tied to a clear purpose, not just vague stockpiling. A savings rate becomes more sustainable when it is connected to a specific financial goal. (Reference: FDIC Money Smart)

Step 5: Start investing to build income-producing assets

Saving creates the foundation, but to go further toward financial freedom, you need to gradually shift part of your money into assets with the ability to grow. At this stage, the goal is not to chase fast returns. It is to build a long-term accumulation system that can grow over time.

When you are just getting started, what matters more than choosing a “hot” investment is understanding how much risk you can handle and how long you can stay invested. A sustainable investment strategy usually depends on discipline, diversification, and the ability to tolerate short-term fluctuations.

Step 6: Increase active income and build additional income streams

If you only optimize spending without improving your ability to earn more, the journey will be slow and may leave you feeling deprived. Increasing your active income through your main job, side skills, or additional work can significantly shorten the road to financial freedom.

In the early stage, extra income does not need to be large. Even so, it creates a very real advantage for saving and investing. Once you have another source of income beyond your main salary, you become less dependent on a single source of support.

Step 7: Review your plan regularly based on real life

A plan that works today may no longer fit a few years from now, because income, family, and life priorities are always changing. That is why, instead of clinging to an old number, you should regularly review your spending, assets, debt, goals, and level of financial autonomy.

Regular reviews help you catch problems early, adjust your pace of saving, and avoid following a model that no longer matches reality. As your income, family situation, and priorities change, you also need to update the way you plan your finances so the journey stays aligned with real life.

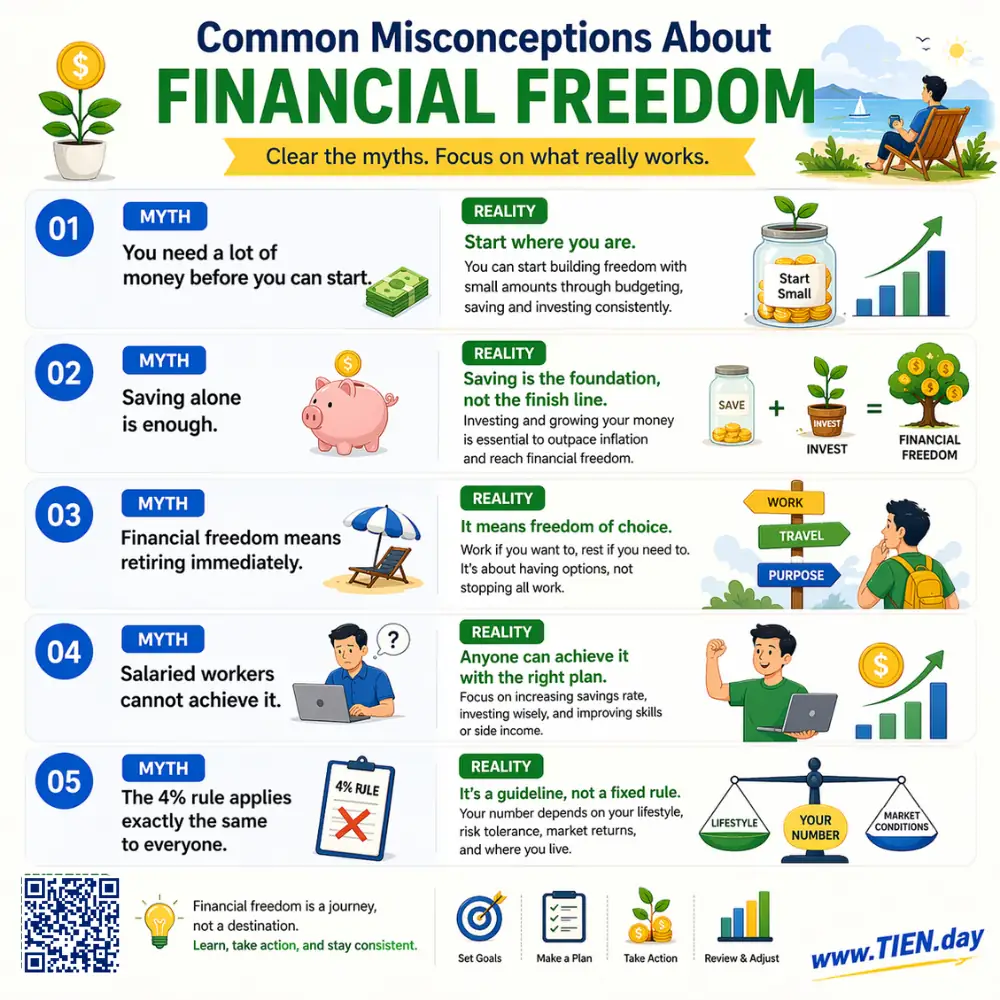

8. Common Misconceptions About Financial Freedom

You need a lot of money before you can start

Many people think financial freedom is only something to talk about once you are already rich, but that belief can be discouraging from the start. In reality, the journey often begins with controlling spending, building a safety buffer, and gradually increasing your level of financial autonomy over time.

Saving alone is enough

Saving is an important foundation, but simply holding cash without accounting for inflation and income-producing assets is a slow path. To move closer to financial freedom, you usually need a combination of saving, risk management, and investing in ways that fit your ability to handle volatility.

Financial freedom means retiring immediately

Another common misunderstanding is that quitting work early automatically means you have achieved financial freedom. In reality, the greater value lies in having the freedom to choose how you want to live, work, and rest without being forced by income pressure.

Salaried workers cannot achieve it

People who earn a salary can absolutely move toward financial freedom if they use the advantage of stable income to save and invest consistently. The difference is not your profession. It is your ability to keep a surplus, build assets, and avoid letting your lifestyle rise faster than your income.

The 4% rule applies exactly the same to everyone

The 4% rule is only a reference point, not a fixed formula for every age group and every market. When using it, you still need to consider inflation, life expectancy, healthcare costs, housing, children, and the real return on your investment portfolio.

9. Can Salaried Employees Achieve Financial Freedom?

Salaried employees can absolutely achieve financial freedom if they know how to make the most of their greatest advantage: steady monthly cash flow. Stable income makes it easier to plan spending, maintain savings, build a safety fund, and allocate money for investment on a more predictable schedule.

A common weakness is that income rises, but lifestyle rises with it, so the actual surplus hardly changes over many years. When lifestyle inflation happens continuously, it becomes easy to feel that you are making progress in salary without truly getting closer to financial freedom.

For most working people in Vietnam, a more realistic approach is not to obsess over retiring early, but to gradually increase financial autonomy over time.

A practical model usually includes three things done in parallel:

- maintain a stable savings rate

- improve skills to increase income

- steadily build income-producing assets

You do not need to start from full financial freedom. You should start by gradually reducing your dependence on a single salary source.

Explore the core system of personal finance foundations.

What Should You Read Next If You Want to Improve Your Financial Freedom?

To improve your financial freedom in a more sustainable way, it helps to keep reading articles that go deeper into specific money behaviors. Taking it one small area at a time makes it easier to understand the issue and apply it in real life at each stage.

- Personal finance management: helps you build a clearer foundation for managing money

- Saving money: useful if your current goal is to build a stable savings habit

- Managing personal cash flow: worth reading if you want to track money coming in and going out more closely

- Financial goals: helps connect daily habits to a specific destination

- Financial psychology: explains how emotions and beliefs shape money decisions.

- Financial Habits: A System for Building a Sustainable Money Foundation

You do not need to read everything at once. Start with the topic that is

Frequently Asked Questions About Financial Freedom

What is the difference between financial freedom and financial independence?

Financial independence usually means you can support your life without needing help from others, but you may still depend on earned income from work. Financial freedom goes further: your assets or accumulated cash flow are enough to support the lifestyle you want, giving you more freedom over your work and time.

Do you need a lot of money to begin this journey?

No. What matters more than starting with a large amount of money is your ability to control spending, create a steady surplus, and build a solid financial foundation. Many people begin this journey by tracking cash flow, reducing high-interest debt, and building saving habits before they think about large assets.

Should you save first or invest first?

For most beginners, it is better to build basic savings first, then gradually increase investing. If you do not yet have emergency reserves and you are still under pressure from short-term debt, investing too early may force you to pull money out midway, making your plan less sustainable.

Is the 4% rule guaranteed to work?

No. The 4% rule is only a reference framework built from historical data, not a guaranteed formula that works perfectly for everyone and every market. When applying it, you still need to account for inflation, retirement age, actual returns, healthcare costs, and family circumstances.

At what age should you start thinking about financial freedom?

The earlier, the better, but there is no age that is “too late” to start. Starting early gives you more time to save, invest, and correct mistakes under less pressure. Starting later can still be meaningful if you follow a realistic and disciplined path.

Conclusion

Financial freedom is not one fixed number that applies to everyone. The right target always depends on your lifestyle, spending needs, family responsibilities, and long-term goals.

More importantly, it is not a state that appears overnight. It is a gradual journey toward greater control over money. The better you manage your cash flow, save consistently, and build income-producing assets, the more freedom you gain in the way you live.

So you do not need to wait until everything is perfect before you begin. What matters more is choosing the right first step, moving forward steadily, and adjusting your plan to fit your real-life circumstances.

References: