Personal Cash Flow: How to Track, Manage, and Improve It

Personal cash flow is the clearest reflection of your financial situation each month. Many people earn a steady income, and sometimes a fairly good one, yet still find themselves short of money near the end of the month. They may not know where their money went or why they were unable to save anything.

The problem is often not just how much you earn, but the fact that you do not clearly see the money coming in, the money going out, and the recurring expenses in between. Without tracking your finances regularly, it is very difficult to assess your spending habits, spot money leaks, or know whether your cash flow is positive or negative.

This article will help you understand what personal cash flow is, why it matters, and how to track, analyze, and improve it effectively. It also serves as a general hub article, giving you a solid foundation before you explore each related topic in more detail.

Nội dung

1. What is personal cash flow?

The concept of personal cash flow

Personal cash flow is the money coming into and going out of a person’s finances over a given period. Understanding your personal cash flow helps you assess your financial situation, track transactions, and see why you end the month with money left over or come up short.

The 3 main components: income, spending, saving, and investing

The three main parts of personal cash flow are money in, money out, and the portion set aside for the future. When you track all three, you can control your spending better and clearly see your ability to save and invest.

Income includes salary, bonuses, side income, and other recurring payments.

Spending includes fixed costs, variable expenses, and unexpected payments.

Savings and investments are the remaining money allocated toward financial goals.

How is personal cash flow different from personal finance management?

Personal cash flow focuses on tracking income, expenses, balances, and short-term changes in your money. Personal finance management is broader. It includes budgeting, financial goals, debt, emergency funds, asset protection, and long-term planning.

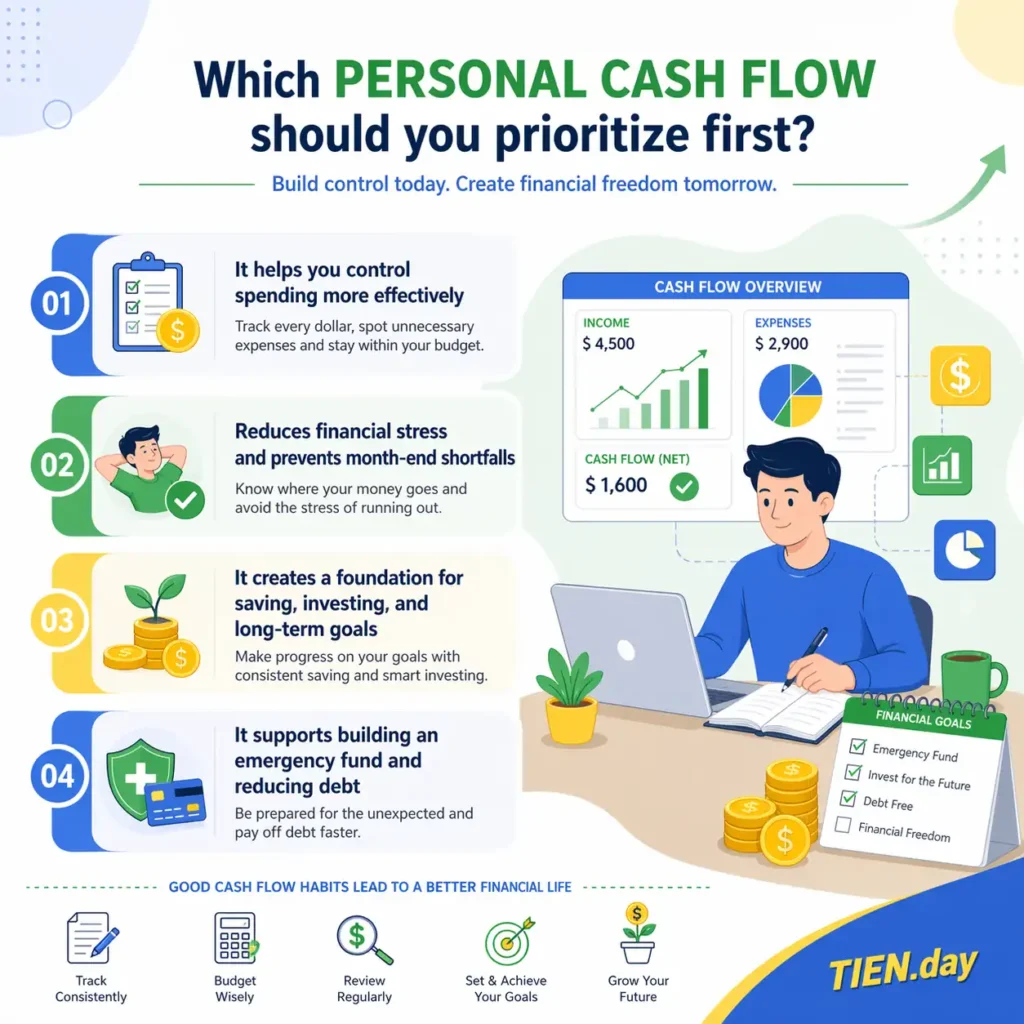

2. Why is managing personal cash flow important?

It helps you control spending more effectively

When you track your personal cash flow regularly, you can clearly see where your money is coming from and where it is going. This helps you manage spending better, spot recurring expenses, and identify which costs are pushing your budget off track.

- Essential expenses are usually easier to manage when they are clearly categorized from the beginning.

- Small expenses that happen repeatedly often create the biggest pressure on your overall finances.

- Recording transactions consistently helps you understand your financial situation instead of just guessing.

Reduces financial stress and prevents month-end shortfalls

One major reason personal cash flow needs to be managed is to reduce money-related stress. When you know how much money you have left, when bills are due, and what your average spending looks like, the risk of coming up short at the end of the month drops significantly.

Better management also helps you make adjustments before your spending exceeds your income. This is an important foundation for understanding what negative cash flow means and changing spending habits early.

It creates a foundation for saving, investing, and long-term goals

If your personal cash flow is not under control, saving and investing usually happen inconsistently. On the other hand, once you understand your income, expenses, and remaining money, it becomes much easier to plan for long-term financial goals.

- Identify how much you can set aside each month.

- Allocate money reasonably between spending, saving, and investing.

- Track progress toward your goals more clearly.

It supports building an emergency fund and reducing debt

Managing personal cash flow also helps you create a safety buffer for unexpected risks in life. When you have a clear picture of the money coming in and going out, it becomes easier to consistently set aside money for an emergency fund and prioritize the debts that need to be paid first.

Over time, this helps make your financial situation more stable and reduces reliance on short-term borrowing.

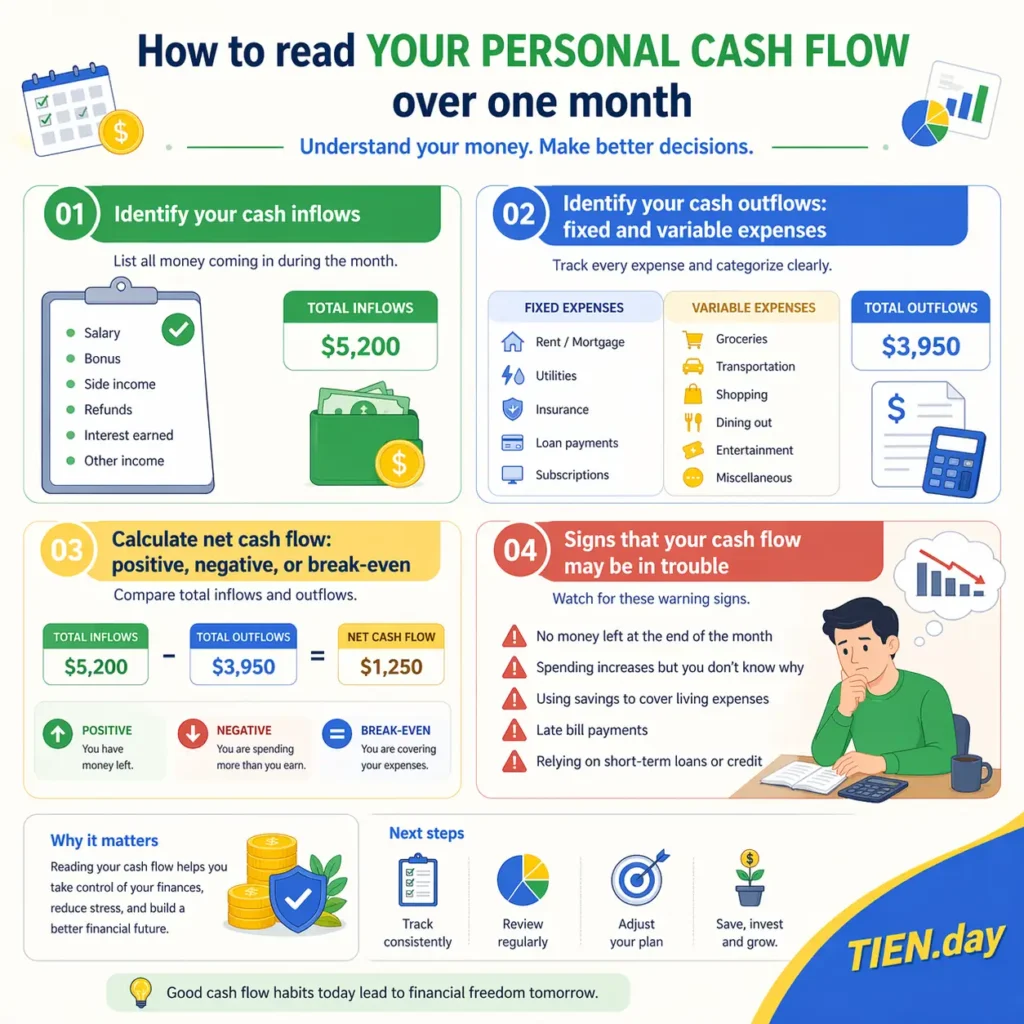

3. How to read your personal cash flow over one month

Identify your cash inflows

To understand your personal cash flow correctly, first gather all sources of money coming in during the month. This usually includes salary, bonuses, side income, refunds, earned interest, and any other incoming transactions.

Identify your cash outflows: fixed and variable expenses

After listing money coming in, the next step is to clearly separate the money going out so you can assess your financial situation more easily. The simplest way is to divide it into fixed expenses and variable expenses, since these two groups reflect how flexible your monthly budget is.

- Fixed expenses include rent, bills, tuition, insurance, and recurring payments.

- Variable expenses include food, transportation, shopping, entertainment, and unexpected spending.

- Proper categorization makes it easier to review your monthly cash flow and adjust costs when needed.

Calculate net cash flow: positive, negative, or break-even

To understand whether your personal cash flow is healthy or weak, you need to calculate the difference between total money in and total money out. If the result is positive, you have money left over. If it is negative, you are spending more than you earn. If the two are nearly equal, you are breaking even.

This is an important step before going deeper into topics like positive cash flow, negative cash flow, and personal cash flow analysis.

Signs that your cash flow may be in trouble

Some warning signs appear early but are easy to ignore. If you spot them in time, you can make adjustments before the shortfall becomes a long-term problem.

- You often have no money left by the end of the month.

- Your spending rises but you do not know why.

- You have to use savings to cover living expenses.

- You pay bills late or rely on short-term borrowing.

If these signs keep repeating, you should review how you manage your cash flow in a more practical way.

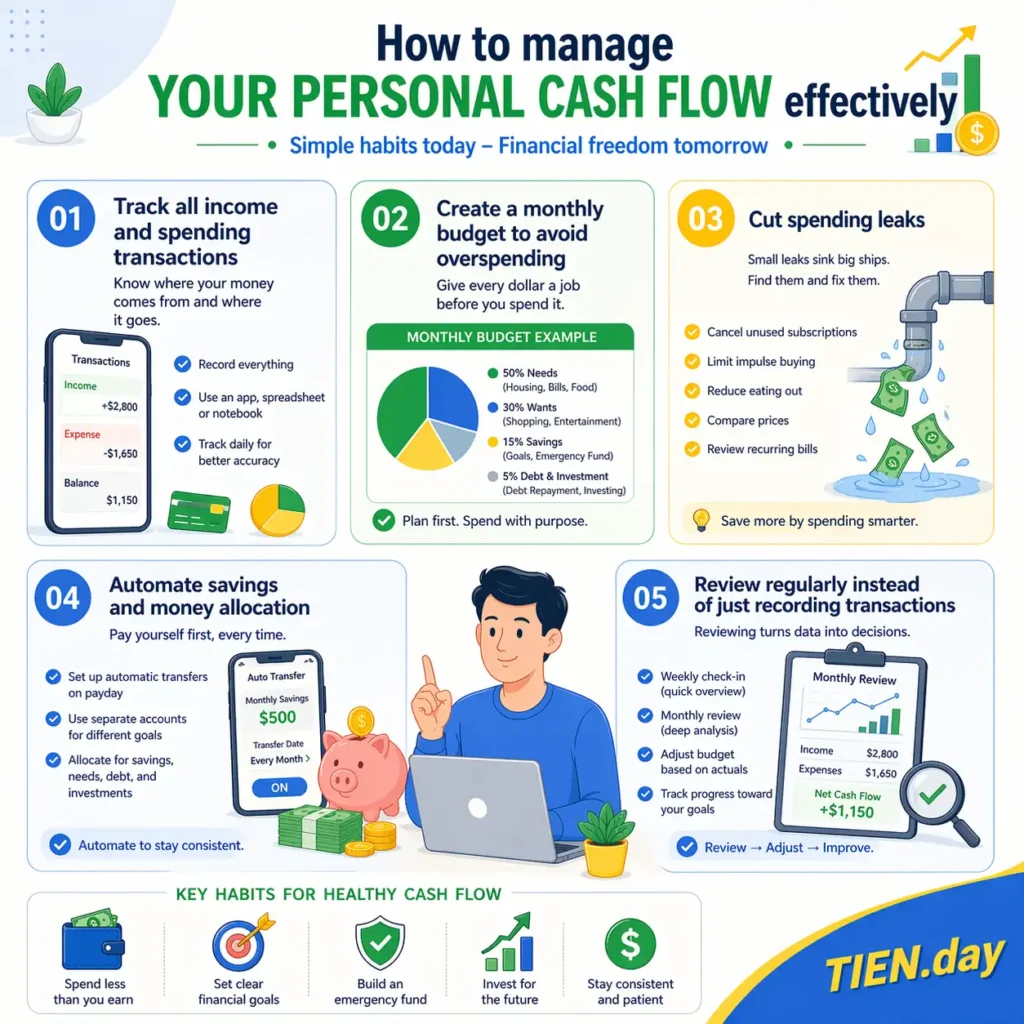

4. How to manage personal cash flow effectively

Track all income and spending transactions

To manage personal cash flow effectively, the first step is to track all money coming in and going out. When transaction data is recorded clearly, you can assess your financial situation more accurately and see where your money is going.

Tracking does not just help control spending. It also helps you spot recurring costs. This is also the foundation for deeper cash flow analysis and building sustainable money habits.

Create a monthly budget to avoid overspending

Once you understand the basic data, the next step is to divide your budget into clear spending categories for the month. This helps your cash flow follow a plan instead of being driven by random transactions.

- Set spending limits for essential needs first.

- Separate savings, debt repayment, and investments at the beginning of the month.

- Keep a small buffer for risks or unexpected expenses.

With a budget in place, it becomes easier to balance current spending with long-term goals.

Cut spending leaks

Many personal cash flow problems do not come from major expenses, but from small costs that repeat over and over. If you do not review them regularly, they will slowly drain your budget and reduce your ability to save.

You should pay close attention to expenses that are not truly necessary, services you barely use but still keep paying for, and emotional spending. Once you control this group of expenses, you will have more room to save effectively and pay off debt faster.

Automate savings and money allocation

One simple way to keep your personal cash flow stable is to automate the money you need to set aside each month. When saving and allocation happen early, you reduce the risk of spending money that should have been kept.

- Transfer savings immediately after receiving income.

- Use separate accounts for spending, emergency funds, and long-term goals.

- Set aside a fixed amount for debt reduction or suitable investments.

Review regularly instead of just recording transactions

Managing personal cash flow does not stop at recording numbers. You also need to review the data regularly and make adjustments. If you only enter transactions without analyzing them, it is hard to notice cost trends, risks, or budget imbalances.

A weekly or monthly review helps you adjust early before shortfalls continue for too long.

5. What should a personal cash flow tracking sheet include?

Key columns to include in a cash flow tracking sheet

A good tracking sheet helps you see your personal cash flow by transaction instead of only looking at your final balance at the end of the month. The structure should be detailed enough to assess your finances, but still simple enough to update consistently.

- Transaction date

- Main category and subcategory

- Short transaction description for easy reference

- Cash in, cash out, and balance after each transaction

- Notes or a small analysis section to identify spending habits

These columns are enough to track income, expenses, transactions, and the money left over during the period.

How to record each transaction accurately

To read your personal cash flow correctly, you should record transactions as close to the time they happen as possible. Delayed updates often lead to missing data, wrong categories, or overlooked small expenses that repeat frequently.

It is best to use one consistent method from the beginning so that weekly and monthly comparisons do not become distorted. A practical approach is to use the same categories, the same currency unit, and the same note-taking rules for every transaction.

Common mistakes when using a tracking sheet

Many people have a tracking sheet but still fail to control their personal cash flow because they only record transactions without reviewing the data. Without a review step, the sheet will not help you identify risks, unusual expenses, or a long-term deficit trend.

- Forgetting cash payments or small transactions

- Putting too many costs into one large category

- Not updating the balance after each transaction

- Not using the data to adjust next month’s budget

When you avoid these mistakes, the tracking sheet becomes a strong foundation for monthly cash flow management and personal cash flow analysis.

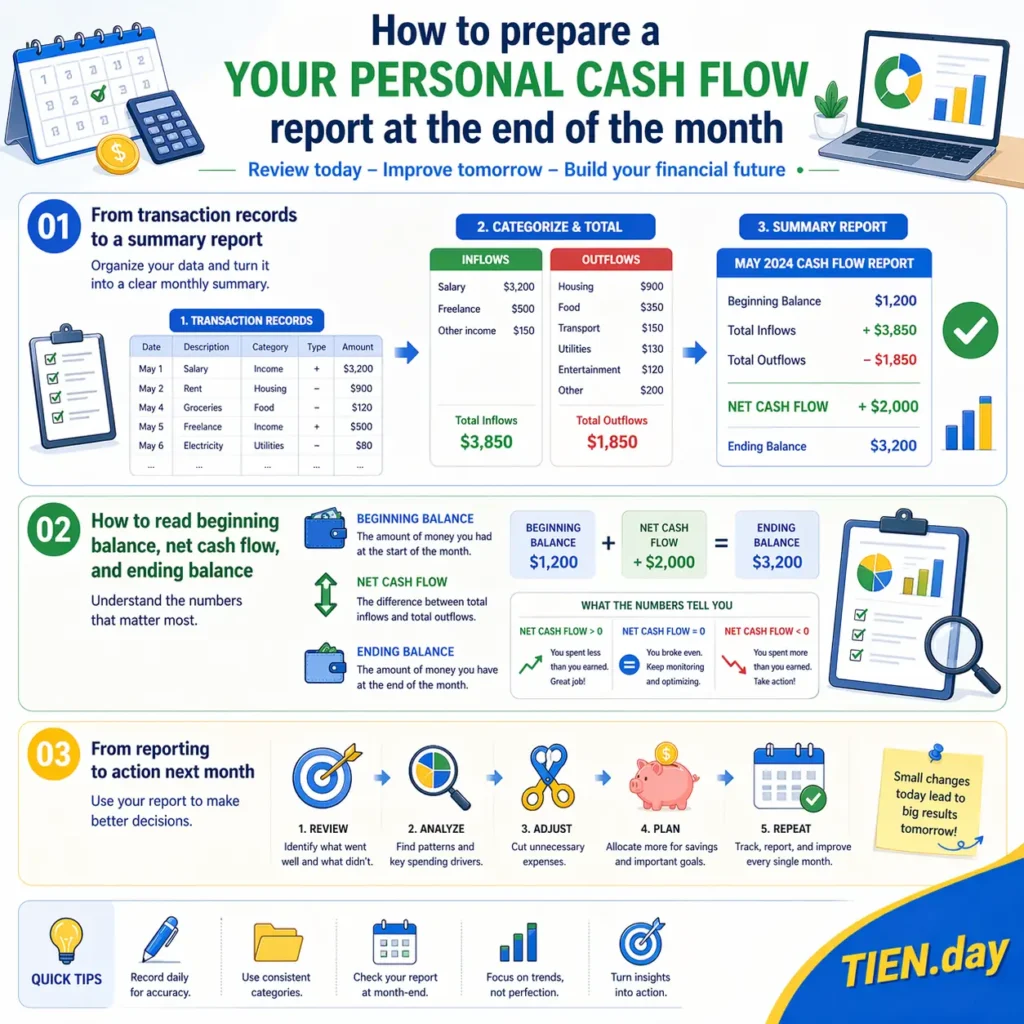

6. How to prepare a personal cash flow report at the end of the month

From transaction records to a summary report

To clearly understand your personal cash flow for the whole month, you need to turn transaction data into a summary report. This report brings together all income, expenses, and remaining money so you can assess your financial situation more clearly.

- Total all cash inflows during the month.

- Add up expenses by major spending category.

- Compare your actual balance with the figures recorded in your tracking sheet.

When done correctly, this helps you identify which expenses are pushing your budget off track.

How to read beginning balance, net cash flow, and ending balance

A personal cash flow report usually needs three basic numbers for a quick and accurate reading: the beginning balance, net cash flow for the period, and ending balance after all expenses.

- The beginning balance is the money you had at the start of the month.

- Net cash flow is the difference between total money in and total money out.

- The ending balance shows how much money is left after all transactions.

If net cash flow is negative for several months in a row, you should review your spending structure.

From reporting to action next month

The greatest value of a personal cash flow report is not the numbers themselves, but the decisions that follow. Once you clearly see your income, spending, risks, and remaining money, you will know what to keep, cut, or adjust in the following month.

7. Comparing personal cash flow and business cash flow

Similarities

Even though they differ in scale, both revolve around tracking money in, money out, and the remaining balance. Both personal and business cash flow require clear transaction data to assess financial health and control costs effectively.

Differences

The biggest difference lies in management goals, complexity, and the level of risk involved. With personal cash flow, the focus is usually on spending, saving, investing, and financial stability. Businesses, on the other hand, also have to manage operations, receivables and payables, inventory, taxes, and working capital.

Individuals usually track income, expenses, emergency funds, and financial goals.

Businesses also need to track revenue, operating costs, debt obligations, and liquidity risk.

Business data often requires reporting, forecasting, and control at multiple levels.

That is why personal finance management should be seen as a system that is much closer to everyday life.

Why individuals should not blindly apply business thinking to personal money management

If you apply business thinking too rigidly, managing your personal money can become overly heavy and difficult to maintain. Personal cash flow management needs practicality, flexibility, and a close connection to real spending habits, rather than too many complex metrics.

A better approach is to keep the core principles but simplify them for personal life.

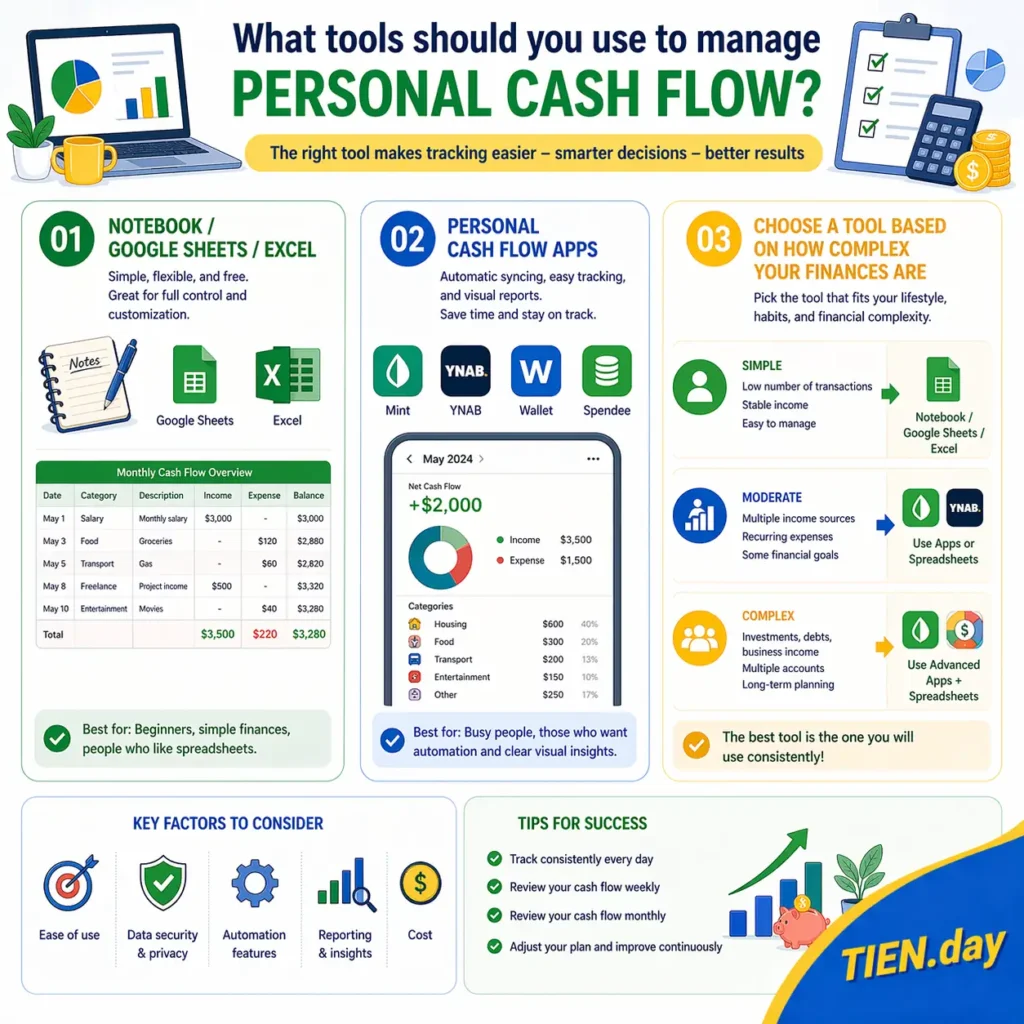

8. What tools should you use to manage personal cash flow?

Notebook / Google Sheets / Excel

If your needs are still simple, you can start with a notebook, Google Sheets, or Excel and track your money consistently. These tools help record your personal cash flow more clearly by transaction, expense category, and remaining balance after each update.

A notebook works well when you have few transactions and a simple tracking style.

Google Sheets and Excel are better when you need calculations, filtering, and monthly budget tracking.

Personal cash flow apps

As your transaction volume increases, apps can make personal cash flow management faster and more visual. Many apps help you record income and expenses, categorize transactions, and view reports directly on your phone.

You can look into apps such as Money Manager, Spendee, expense tracking apps, or digital banking apps. For more advanced needs, articles about personal finance apps and budgeting tools may be more useful.

Choose a tool based on how complex your finances are

No single tool works for everyone, because transaction volume and financial goals vary from person to person. If your personal cash flow is still simple, a spreadsheet may be enough. If your data becomes more complex, an app may be more convenient.

What matters most is not using the most advanced tool, but choosing one that is easy enough to stick with consistently.

Frequently asked questions about personal cash flow

What is positive cash flow?

Positive personal cash flow means the total money coming in during a period is greater than the total money going out. In other words, you still have money left after spending. This is a good sign because it creates a foundation for saving, emergency funds, debt repayment, and investing.

Is negative cash flow dangerous?

Negative personal cash flow is not always immediately dangerous, but if it continues for many months, it becomes a serious warning sign. It means you are spending more than you earn, which can drain your savings, increase financial pressure, and slow down your long-term goals.

How often should you review your cash flow?

You should review your personal cash flow weekly at a basic level and do a full summary monthly so you can spot budget problems earlier. If your finances involve many transactions, multiple income sources, or many fixed expenses, you should review it more often.

Should you use an app instead of Excel?

You can use an app instead of Excel if you want faster and more convenient cash flow tracking on your phone. However, the best option depends on your habits, the complexity of your finances, and whether you can keep it updated consistently each week.

Conclusion

Understanding personal cash flow is not just about knowing how much you earn. It is also about knowing where your money goes each month. When you clearly track money in, money out, and what remains, you can assess your financial situation more accurately and make better spending decisions.

More importantly, good personal cash flow management helps you avoid running short at the end of the month, control spending leaks, and build a foundation for saving, emergency funds, and long-term goals. It is a practical skill that needs to be maintained consistently, not just for a short time.

From here, you can go deeper into topics such as how to manage cash flow and what negative cash flow means in order to handle specific situations.

See more: Personal financial planning: How to create a clear and easy-to-implement plan

Vietnamese: Dòng tiền cá nhân: Cách theo dõi, quản lý và cải thiện

Reference: