Personal Finance Management: A Path to Financial Freedom

Many working people share the same feeling: their income is not too low, they work hard, but by the end of the month, there is not much money left.

The problem is often not only about salary. It is also about personal finance management and how cash flow is used every day.

When you cannot clearly see where your money comes from, where it goes, and which expenses are quietly draining your budget, it becomes very difficult to save or move closer to bigger financial goals.

This article is an overview page designed to help you assess your current financial situation more clearly, understand what personal finance management includes, and see why it is the foundation of saving, investing, and long-term financial stability.

From there, you can choose an approach that fits your situation and know what to read next to manage your income and expenses more effectively.

Nội dung

1. What Is Personal Finance Management and Why Is It an Important Foundation?

What is personal finance management?

Personal finance management is the process of controlling your income, spending, savings, investments, and financial protection so your money is used with more purpose. It is not only about cutting expenses. It is about organizing your entire cash flow so you can cover your current needs, prepare for long-term goals, and handle unexpected risks.

How is personal finance management different from expense tracking?

Expense tracking is only one part of the bigger picture. With personal finance management, you do not just track what you spent. You also build a budget, prepare an emergency fund, set financial goals, manage debt, and allocate money in a way that fits your real situation.

In other words, expense tracking helps you see the money going out, while personal finance management helps you see the full system: money coming in, money going out, and the amount left for saving and investing. This broader view is what creates a strong foundation for long-term financial stability.

Why do many people with good income still run out of money at the end of the month?

Many people do not run short at the end of the month because their income is too low. The real issue is often that money comes in regularly, but there is no clear system for managing it. When you do not review your current financial situation and do not know which costs are fixed and which are emotional or unnecessary spending, small repeated expenses can slowly drain your budget every month.

Another reason is that many people focus only on earning more money, but they do not build a spending plan, set aside money for emergencies, or connect their money to clear goals. Before going into methods and tools, it is important to understand personal finance management as the foundation for making better money decisions.

2. What Does Personal Finance Management Include?

Income

The first foundation of personal finance management is understanding all the money you have coming in each month. You should list your main income, side income, active income, and passive income so you can see your real cash flow clearly.

Signs that you understand your income include knowing how much you earn, where the money comes from, which income sources are stable, and which ones change from month to month.

If you do not clearly understand your income, it becomes very hard to build a realistic budget or set practical goals.

Spending

The next part of personal finance management is tracking your spending by category so your money does not feel vague or confusing. A simple way is to separate fixed expenses from variable expenses, then divide them into needs and wants.

Spending includes rent, utilities, food, transportation, insurance, shopping, entertainment, and small unexpected expenses. When you understand your spending structure, you can see which areas need attention first instead of cutting randomly or spreading your efforts too thin.

Saving

Saving helps create a safe zone for your future. Instead of saving money in a general way, you should divide it into short-term savings, an emergency fund, and goal-based savings. When your savings have a clear structure, you can handle plans and unexpected costs with more confidence.

Investing

Investing is the pillar that helps your wealth grow. However, investing should come only after you already have a stable money management foundation. If you have not controlled your spending and do not have an emergency fund, investing too early can create major risk. Investing is an extension of personal finance management, not a replacement for it.

Financial protection

The last part, but a very important one, is protecting yourself from unexpected risks. An emergency fund, the right insurance, and avoiding bad debt can keep your financial plan from falling apart because of one surprise event.

Without this layer of protection, all your efforts to manage income, spending, and savings can easily be interrupted. Personal finance management is not only about organizing money today. It is also about protecting your stability tomorrow.

If you do not know where your money goes each month, it is almost impossible to manage your personal finances effectively.

3. Core Principles for Effective Personal Finance Management

Spend less than you earn

This is the most basic principle of sustainable money management. If you spend more than you earn for many months, it becomes difficult to build a stable budget, save money, or avoid depending on short-term debt.

A quick check is to compare your total income and total expenses over the past month. If the gap is very small or negative again and again, your personal finance system is not strong enough yet.

Pay yourself first

Instead of waiting to save whatever is left after spending, set aside part of your income as soon as you receive it. This makes your budget clearer and turns saving into a priority instead of an afterthought.

A simple checklist for this principle:

- Separate your savings money from spending money

- Set up automatic transfers

- Do not use goal-based savings for everyday expenses

This is a simple step, but it is very helpful if you want to manage your finances more consistently.

Always have an emergency fund

An emergency fund is the buffer that protects your plan when surprise expenses happen. It can help cover unexpected repairs, medical bills, or temporary income loss.

Without this fund, many people are forced to borrow money or use funds meant for other goals. That is why building an emergency fund should come before focusing too much on investment returns.

Track before you optimize

You cannot improve what you do not measure, and money works the same way. Before cutting expenses or optimizing your budget, write down your income and expenses so you can clearly see your real spending patterns.

A useful checklist:

- Record income sources

- Record fixed expenses

- Record variable expenses

- Record small repeated daily costs

Tracking helps you understand the real problem before trying to fix it based on feelings.

Automate your savings

Automatically moving money into savings helps you rely less on willpower. When saving becomes part of a fixed process, it is easier to maintain and harder to skip because of unnecessary spending.

Manage money based on goals, not emotions

Money should be connected to clear goals instead of emotional decisions in the moment. When your financial goals are clear, you can see what should come first, what can wait, and what needs limits.

A simple way is to separate short-term goals, your safety fund, and long-term goals into different groups. This makes your budget more aligned with your real priorities and helps your financial management stay consistent over time.

Review and adjust regularly

No financial plan stays the same forever because income, needs, and life circumstances change. Good personal finance management requires regular review so you know what is working and what needs to be adjusted.

A simple monthly checklist:

- This month’s income

- Actual spending

- Savings progress

- Any category that went over budget

4. How to Start Managing Personal Finances with a Simple Process

Step 1: Review your current financial situation

The starting point is to see your real financial picture clearly instead of guessing. Add up your total income, required expenses, debts, and the amount of money you actually have left at the end of each month.

A simple checklist:

- Know how much you earn

- Know what bills or payments you are responsible for

- Know how much usable money is left

If you do not understand your current situation correctly, it is very easy to build the wrong spending plan from the start.

Step 2: Track your spending for 30 days

Once you understand the big picture, track your spending for at least 30 days. The goal is not to be perfect right away. The goal is to see where your money goes and which expenses happen more often than you realize.

You can use a notebook, Excel, or an app. What matters is doing it consistently and clearly. In personal finance management, real data is always more useful than the feeling that you “probably do not spend that much.”

Step 3: Categorize expenses and build a budget

After you have spending data, the next step is to group your expenses so they can fit into a budget. Separate fixed expenses from variable expenses, then divide them into essential and non-essential spending.

A basic checklist:

- Rent

- Utilities

- Transportation

- Food

- Debt payments

- Shopping

- Entertainment

From there, you can build a practical budget that fits your real life instead of distributing money randomly.

Step 4: Set goals and build an emergency fund

A sustainable personal finance process does not stop at controlling monthly spending. You should build your emergency fund first, then divide money into short-term, medium-term, and long-term goals based on priority.

This helps each amount of money have a clear purpose and reduces the chance of mixing funds for different goals. When your emergency fund and goals are clear early on, effective personal finance management becomes much easier to maintain.

Step 5: Review and adjust every month

The final step is to review your plan regularly and see whether it still matches real life. Compare income and expenses, check whether you are running a deficit, and identify any category that is over budget or moving away from your original goals.

Monthly reviews make personal finance management more flexible when your income, needs, or financial pressure changes. This helps you not only track money better, but also adjust in time based on your real situation.

5. Common Personal Finance Management Methods — Which One Should You Choose?

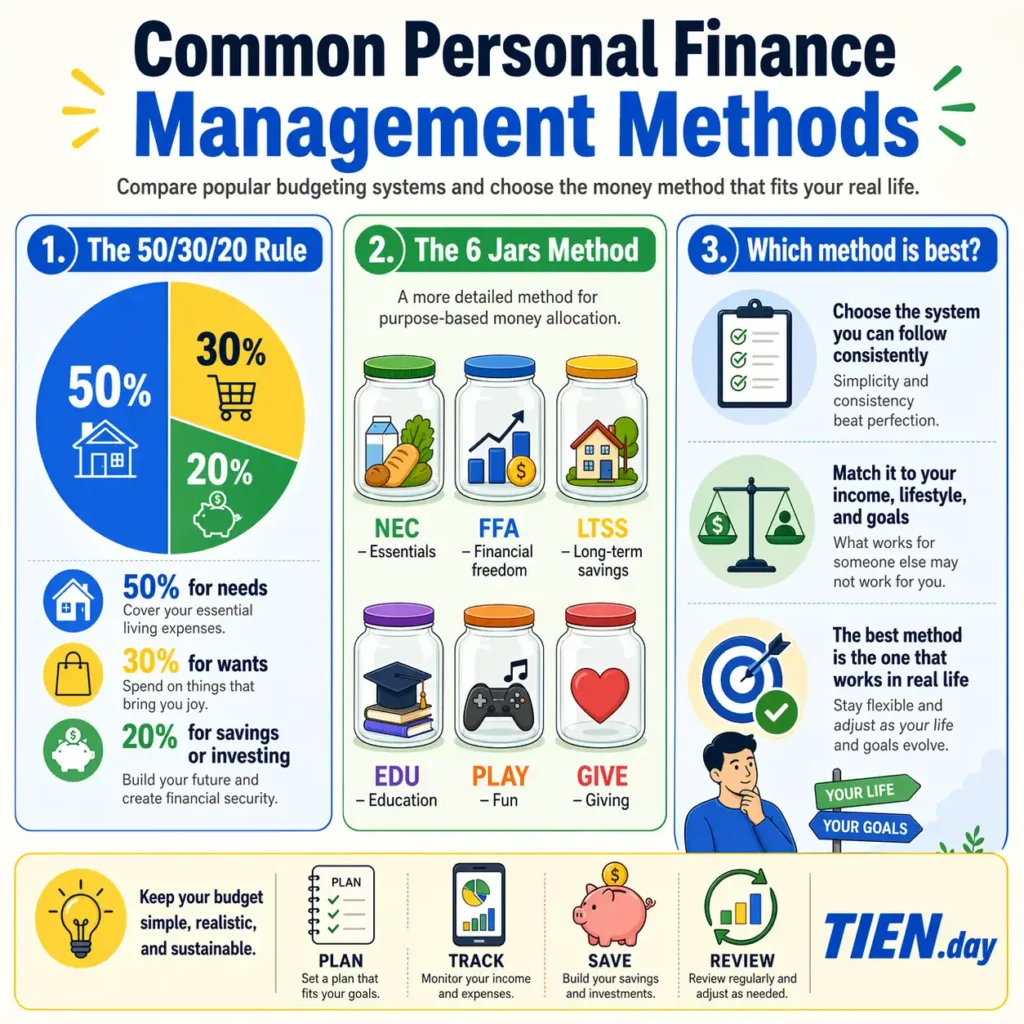

The 50/30/20 rule

Among common budgeting methods, the 50/30/20 rule is a simple and easy-to-understand framework. It suggests:

- 50% of income for needs: rent, food, transportation, bills

- 30% of income for wants: entertainment, shopping, travel

- 20% of income for savings or investing

This method is often a good fit for beginners because it has a clear structure, is easy to follow, and does not require too much detail. Still, it is only a reference point, not a fixed formula that works for everyone.

The 6 jars method

The 6 jars method is a more detailed approach than the 50/30/20 rule. Instead of dividing income into three broad groups, it splits money into smaller funds for essential spending, financial freedom, long-term savings, education, fun, and giving.

- NEC (55%) – essential expenses

- FFA (10%) – financial freedom

- LTSS (10%) – long-term savings

- EDU (10%) – education and learning

- PLAY (10%) – enjoyment and fun

- GIVE (5%) – giving and charity

The difference is that the 6 jars method works better for people who like clear control over each purpose of their money. The downside is that it requires more discipline and may feel too complicated if your income is unstable or your living costs change often.

You can read more in separate articles about the 50/30/20 rule and the 6 jars method to decide which one fits you better.

No method is right for everyone

The most important point is that no formula works perfectly for every person at every life stage. Income is different, living costs are different, and financial pressure is different. Your money system should match your real life, not force you to follow a nice-looking ratio in theory.

A quick checklist for choosing the right method:

- Your current income

- How stable your cash flow is

- Debt pressure

- Your saving ability

- Your upcoming goals

When you look at these factors together, it becomes easier to choose a money system that fits your situation instead of following a general model.

In personal finance management, the real value is not choosing the most famous method. The real value is whether that method helps you keep your budget clear, steady, and sustainable in your real life.

6. Important Topics in the Personal Finance Management Cluster

If you want better control over spending

After understanding the basics of personal finance management, many people need to go deeper into content that helps them control daily money better. This is the right path if you want to know where your money goes, which categories are going over the limit, and how to organize your budget more clearly.

You should continue in this order:

- How to track spending

- How to create a personal budget

- Spending: how to manage, control, and allocate money effectively

These three topics help you move from observing your cash flow, to identifying problems, to building a more practical spending system. If your biggest problem right now is not knowing where your money went at the end of the month, this is the group of content to prioritize first.

If you want to manage money based on life situation and personal context

Not everyone can use the same financial method because income, responsibilities, and financial pressure are different for each person. In personal finance management, choosing the right article for your real situation is often more useful than trying to apply one general formula to everyone.

A quick guide for this group:

- How to manage salary income

- Personal finance management for young professionals

- Family finance management

- Managing money on a low income

- Money management for students

- Money management when running a business

If you are in a very specific stage of life, start with the article that matches your situation first. This makes personal finance management feel less general and more practical.

If you want to avoid mistakes and build a stronger long-term system

Once you have basic control over income and spending, the next step is to avoid repeating mistakes and build a more durable money system. This is when you should read content that connects personal finance management with planning, goals, and long-term cash flow instead of looking only at short-term spending.

You can continue with:

- Common money management mistakes

- Personal financial planning

- Financial goals

- Personal cash flow

- Financial knowledge and skills

If you want to take action more quickly, you can also use a personal finance spreadsheet, an Excel file, or tools that help track your money. This group of content is useful when you want to move from understanding concepts to taking regular, structured action every month.

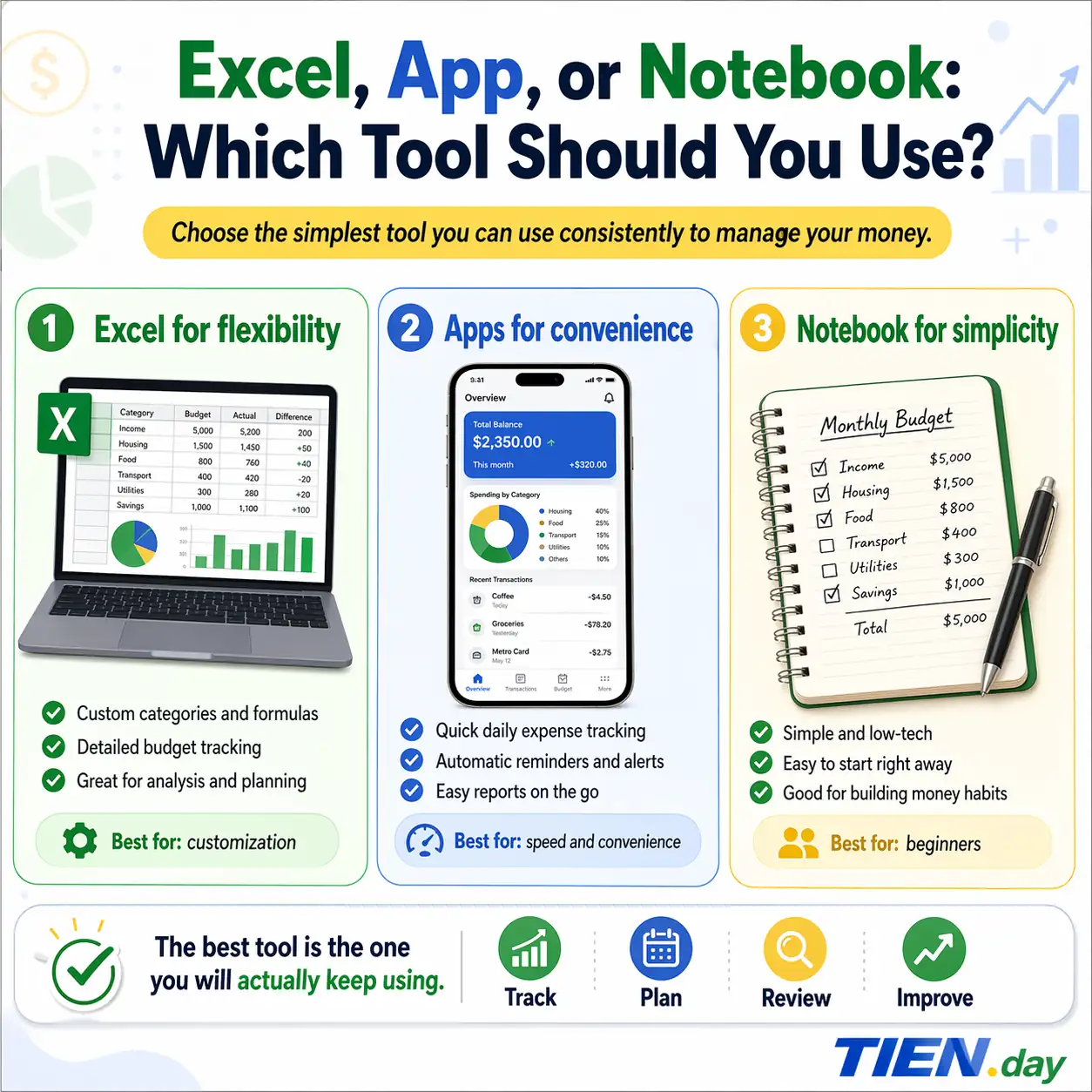

7. Should You Use Excel, an App, or a Notebook for Personal Finance Management?

Besides the method you use, the tracking tool also has a big effect on whether you can maintain the habit over time. In personal finance management, Excel works well for people who like to customize their tracking system and analyze income, spending, budgets, and financial goals in more detail. Finance apps are convenient for busy people because they allow quick entry, visual reports, and automatic reminders. A notebook is better for beginners or people who want a simple tracking system without relying on technology.

In reality, there is no single best tool for everyone. If you want flexibility and like seeing numbers clearly, Excel may be the best choice. If you want speed and something easy to maintain every day, an app may be more practical. If you want to build the habit from the most basic level, a notebook is still a simple and effective option.

Download the free personal finance management file (basic version)

Download the free personal finance management file (premium version)

Frequently Asked Questions About Personal Finance Management

-

Where should personal finance management start?

You should start by understanding your current financial situation clearly: your income, necessary expenses, debt, and the amount of money you have left. When you understand how your cash flow works, you can build a budget, set goals, and make better financial decisions.

-

Can you manage your finances if your income is low?

Yes. Personal finance management does not require a high income to begin. It requires knowing what to prioritize first. With a low income, the main focus is usually on controlling spending, avoiding bad debt, and building a small but steady saving habit.

-

Should you save first or invest first?

In most cases, you should focus on saving and building an emergency fund before investing. If your financial foundation is not stable yet, investing too early can force you to withdraw money too soon or create more financial pressure when unexpected problems happen.

-

Do you need to use an app or Excel?

Not necessarily. An app, Excel, or a notebook is only a tool. What matters most is whether you can track your money consistently and understand your cash flow. Choose the simplest method that you can maintain over time instead of using a tool that feels too complicated.

-

How often should you review your finances?

For most people, once a month is a good schedule. It is frequent enough to catch problems early, but not so often that it becomes stressful. If your income is unstable or you are trying to control spending more tightly, you can also review it weekly.

Conclusion

Personal finance management is the foundation that helps you use money with purpose instead of letting it be shaped by habit and emotion. When you clearly understand your income, spending, emergency fund, and financial goals, it becomes easier to make better decisions and reduce financial stress in daily life.

However, this is not the end point. It is only the beginning of a more sustainable financial system. From this foundation, you can continue improving your budget, managing your cash flow, and building long-term goals that fit your real-life situation.

Vietnamese: Quản lý Tài chính Cá nhân

Reference

- CFPB – Budgeting: How to create a budget and stick with it

- HSBC – Steps to personal financial management

- Tạp chí ngân hàng – Quản lý tài chính cá nhân: Vai trò của lập ngân sách và tiết kiệm tài chính