Saving money: Easy ways to start and maintain effectiveness

Saving money is a very common goal, but not everyone knows where to start. Many people earn a steady income every month yet still end up with very little left, simply because they have not found a way to manage money that fits their financial situation.

The problem is often not that you earn too little, but that you do not clearly see where your money is going, do not have a specific goal, and have not built a consistent saving habit. As a result, the more you rely on motivation or impulse, the more likely you are to give up halfway.

This article will help you understand saving the right way, choose a saving method that matches your current income, and build a simple system you can maintain over time. When you are on the right track, setting money aside becomes more practical, more sustainable, and less stressful, while also creating a stronger financial foundation for the future.

Nội dung

1. What Saving Money Means and Why It Is the Foundation of Personal Finance

What is saving money?

Saving money means intentionally setting aside a portion of your current income for future needs. Unlike extreme cutbacks, saving money does not require you to give up every expense. Instead, it focuses on allocating your money reasonably based on your goals and actual circumstances. This is an important part of personal financial management because it helps you build a financial cushion instead of constantly living close to your spending limit.

Why saving money matters

When you build a habit of saving money, it becomes easier to create an emergency fund to deal with unexpected costs such as losing a job or paying for repairs. Beyond emergencies, accumulated savings also help you pursue both short-term and long-term goals without relying too much on borrowing.

At its core, saving money helps reduce psychological pressure when disruptions happen, while also creating a more stable foundation for future financial decisions, including:

- Having an emergency fund for unexpected situations

- Having money set aside for short-term and long-term goals

- Reducing dependence on debt and cash flow pressure

When should you start saving?

You do not need to wait until your income is high to start saving, because in the early stage, habit usually matters more than the amount. A reasonable approach is to begin with a small, steady amount that fits your current cash flow, then gradually increase it as your financial situation becomes more stable.

Many consumer finance guidelines that help save time suggest the same basic approach: start early, set clear goals, and stay consistent instead of forcing yourself to save too much and then giving up halfway.

2. Why Many People Want to Save but Still Cannot Put Money Aside

Not knowing where the money is going

Many people think they do not spend much, but they do not have clear data to verify that. When you do not track your spending consistently, it becomes very difficult to know which expenses are getting in the way of your saving goal and pulling your budget off track.

Not having a specific savings goal

A common reason is that many people want to set money aside but have not defined a clear savings goal. When you do not know whether you are saving for an emergency fund, a short-term goal, or a long-term plan, it becomes harder to stay motivated and harder to decide how much you should set aside each month. No idea where their money is going

Saving based on impulse instead of using a system

Many people only save when they happen to have money left over at the end of the month, so their progress is often inconsistent. This approach easily leads to a cycle of remembering one month and forgetting the next, while sustainable saving usually requires a clearer system, such as:

- Tracking actual spending instead of estimating

- Setting a fixed amount to save each month

- Separating savings from your everyday spending account

Spending on things that are not truly necessary

When you do not have clear financial priorities, it is very easy to spend on things that are not really necessary without noticing. Over time, it is often these small repeated expenses that slow down your savings plan, even if your income does not change much.

3. How to Start Saving Money as a Beginner

Step 1: Define a clear savings goal

If you want to save money effectively, you should begin with a specific goal instead of just vaguely thinking about setting money aside. The clearer the goal, the easier it becomes to determine how much you need, how long it will take, and how much priority it should have in your personal financial plan. You can divide your goals into familiar categories such as an emergency fund, education, travel, buying a vehicle, or debt repayment so that tracking becomes more practical.

Step 2: Review your current financial situation

Once you have a goal, you need to look at your current financial situation to understand where you stand. Before creating a savings plan, review the following:

- Your monthly take-home income

- Fixed expenses such as housing, utilities, and transportation

- Variable expenses such as food, entertainment, and shopping

- Debt or financial obligations that must be paid regularly

Once you know these numbers, you will understand how much money is actually left and avoid setting a plan that is beyond your capacity. Budgeting guidelines also recommend using bank statements, bills, and actual spending data to get an accurate picture of your finances.

Step 3: Choose an appropriate amount to save

Beginners often make the mistake of setting a savings rate that is too high, then quickly giving up after only a few months. A safer approach is to choose a savings amount that fits your current income, one that you can maintain consistently, then gradually increase it as your cash flow becomes more stable. The important thing is not to start big, but to start realistically so you can build a more sustainable saving rhythm over time (MoneySmart).

Step 4: Save first, spend later

Once you determine the amount to set aside, you should treat it as a required part of your monthly budget. This approach makes saving less dependent on emotion and reduces the risk of spending everything before thinking about saving. Instead of waiting until the end of the month to see what is left, you should separate your savings as soon as you receive your salary or any stable income.

Step 5: Automate your savings

To stay consistent, you can use an app to automatically transfer money into a savings account as soon as you get paid or receive stable income. This helps reduce manual decision-making, saves time, limits impulse spending, and makes saving money a clearer habit in daily life. To implement this more effectively, you can:

- Separate your spending account and savings account

- Set a fixed transfer schedule each month or each payday

- Review regularly and adjust when your income changes

4. Tips: 10 Practical and Easy Ways to Save Money Every Day

Track your spending to spot money leaks

If you want to save money more sustainably, you need to know where your money is going each day. When you track your spending consistently, it becomes easier to identify repeated expenses, adjust your budget, and reduce the items that are slowing down your savings goals.

Cook at home and eat out less

Eating out often increases costs quickly because it comes with drinks, delivery fees, and many small extra charges. If you want to save money every day, cooking at home is an easy method because it helps you control both cost and how often you buy extra things outside your plan.

Delay purchases before deciding to buy

Even a small expense can create long-term pressure if it is repeated too often based on emotion. Before making a purchase, you should create a short pause to ask whether the item is truly necessary or just a temporary desire.

Cut back on subscriptions you rarely use

Many people lose money every month on services that are still auto-renewing even though they barely use them anymore. If you want tighter personal financial management, you should review recurring subscriptions and remove the ones that no longer fit your current needs.

Compare prices before buying

Comparing prices is not just about looking at the listed price, but also about understanding real value on the same unit of use. When you compare unit prices, discounts, and equivalent alternatives, you can buy more wisely and reduce unexpected extra costs.

Take advantage of promotions, but do not buy impulsively

A promotion is only useful if the product was already part of your spending plan. If you buy something extra just because it is discounted, you are still spending money rather than truly saving in a way that benefits your overall cash flow.

Quick checklist:

- Check whether you truly need the item before chasing deals

- Stick to a fixed shopping list when paying

- Skip the promotion if the item is not one of your current priorities

Reuse items while they are still suitable

Not every saving opportunity comes from cutting expenses immediately. When an item is still usable, repairing it slightly, reusing it, or giving it a new function can help you delay replacing it and keep your budget more stable.

Limit borrowing to reduce financial pressure

Borrowing is not wrong in every case, but debt reduces the amount of money left for saving. If you want to set money aside more consistently, you should prioritize controlling debt and avoid taking on new obligations beyond your repayment ability (MoneyHelper).

Increase income to increase saving capacity

In many cases, cutting expenses alone is not enough if the gap between income and costs is too small. If you want to save money more effectively, you can work on optimizing spending while also looking for ways to increase income that fit your available time and current skills.

Use tools or apps to maintain discipline

Not everyone can stick with a notebook or manual spreadsheet for a long time. For many people, using tools to track spending, create budgets, or divide money into goal-based categories helps them save more consistently and maintain discipline month after month.

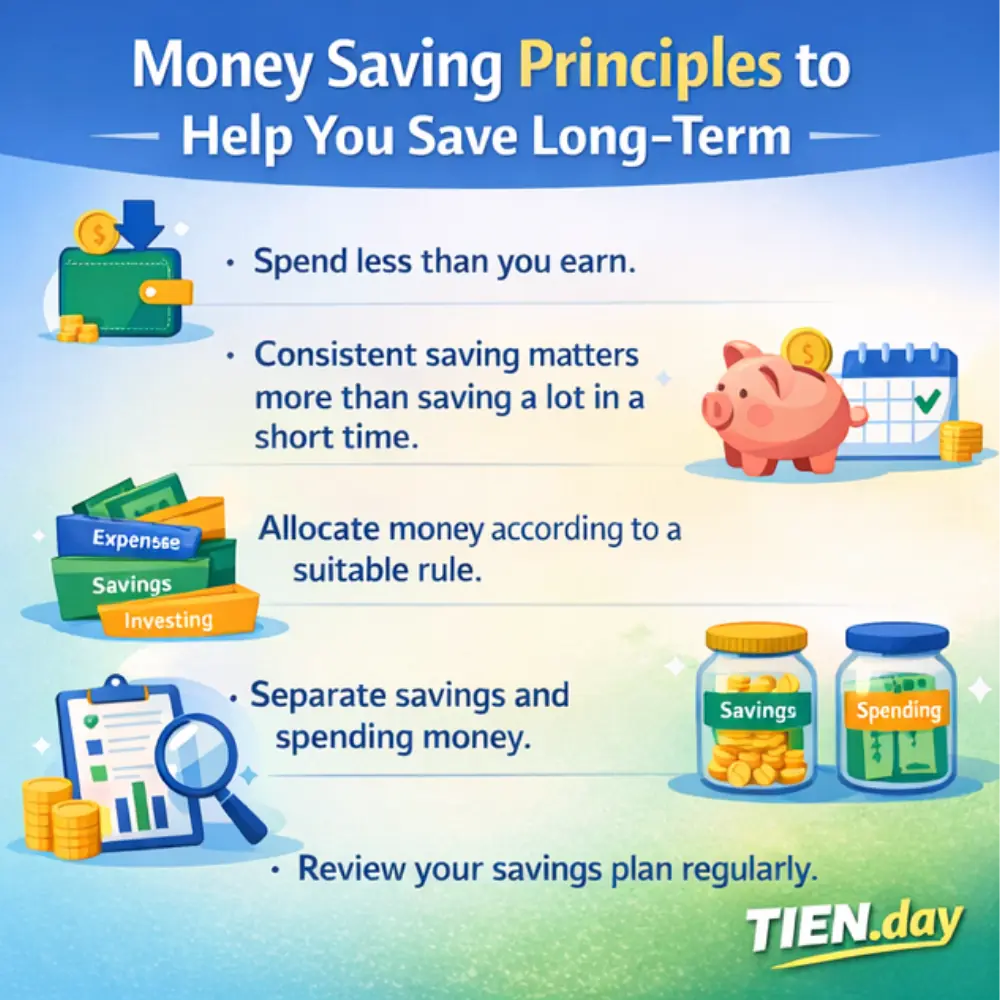

5. Saving Principles That Help You Stay Consistent Over Time

Spend less than the money you have

The most basic principle for long-term saving is to spend less than your actual monthly income. When your total spending exceeds the money you have, your savings plan becomes easy to interrupt and much harder to turn into a stable financial foundation.

Saving consistently matters more than saving a lot in a short time

Many people start with strong determination, but quickly give up because they set the amount too high. In reality, saving money at a steady pace that fits your situation is usually more sustainable than trying to save a large amount in a short period and then losing motivation.

Divide your money using a rule that fits

To make saving easier to maintain, you can divide your income using a simple management framework instead of spending emotionally. Two common methods are the 50/30/20 rule and the six jars method, but in the early stage, what matters more is choosing a system that fits your cash flow and current goals.

Separate savings from spending money

One practical rule is not to keep your savings mixed with your daily spending money. When you separate accounts or funds, it becomes easier to track progress and reduce the chance of dipping into savings for poorly considered expenses.

Review your savings plan regularly

A savings plan should not be created once and then left unchanged for months. You should periodically review the following:

- Check your current income and spending level

- Compare actual progress with your savings goal

- Adjust the amount you save when your financial situation changes

Regular review makes your plan more flexible, more realistic, and more sustainable over time.

6. Which Saving Method Should You Choose Depending on Your Situation?

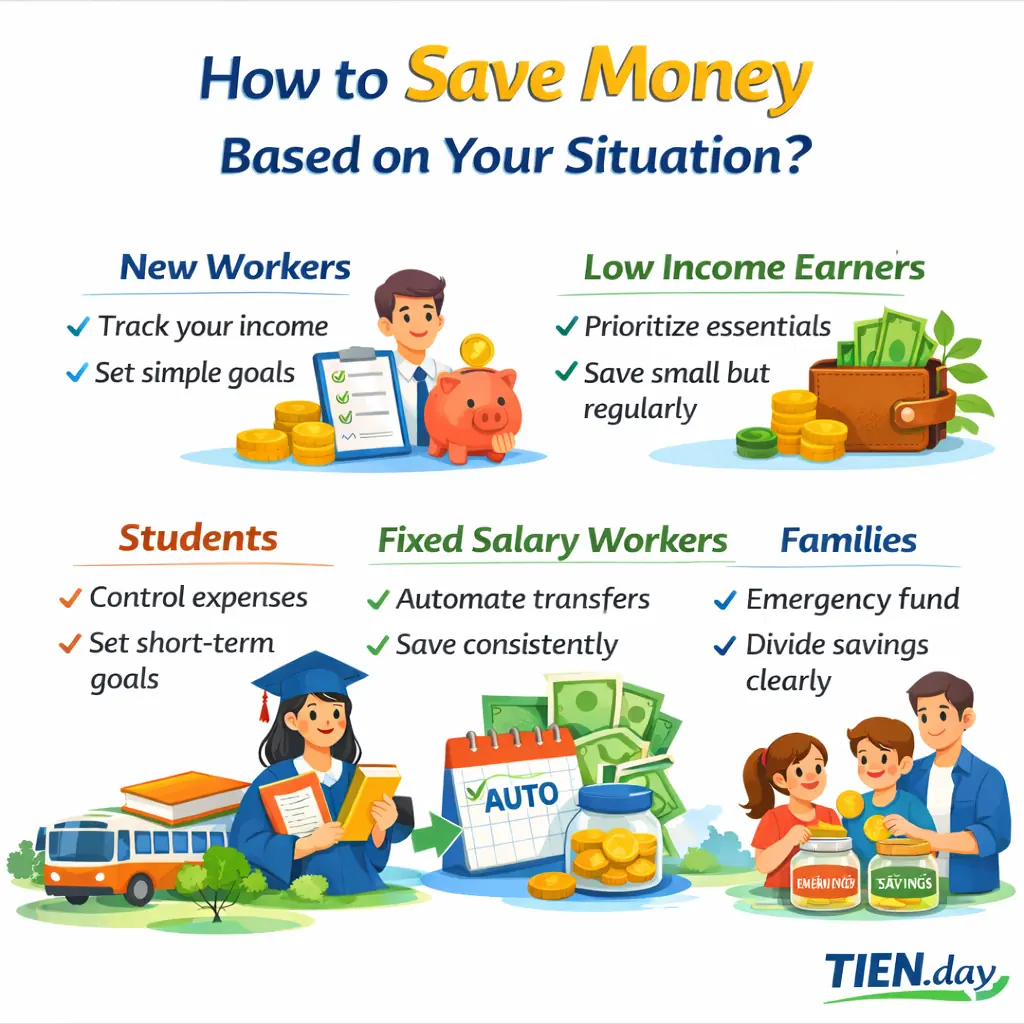

How should new workers save money?

For people who are just starting work, the most important thing is to build the habit before trying to save a large amount each month. You should begin by tracking your income, fixed expenses, and setting a simple savings goal that you can maintain consistently from your first few months of working.

How should low-income earners get started?

If your income is still limited, you should not force yourself into a rigid ratio that creates pressure and makes you give up. A more suitable approach is to prioritize essential spending, cut expenses that are not truly necessary, and save a small but steady amount so that your savings plan remains realistic (MoneySmart).

How can students save money?

For students, saving money is usually more effective when it starts with managing small expenses and having clear short-term goals. You should control study-related costs, transportation, food spending, and avoid spending based on impulse, because at this stage financial discipline matters more than building a large amount of savings.

Should people with a fixed salary save monthly or automate transfers?

If you have a fixed salary, the easiest way to stay consistent is usually to transfer money on schedule as soon as you get paid rather than waiting until the end of the month. This method makes saving less dependent on emotion and helps accumulation happen more steadily according to plan.

How should families divide their savings funds?

For families, a reasonable approach is to divide money by purpose so that it is easier to track and less likely to get mixed across priorities. You can begin with a short checklist:

- Separate the emergency fund from goal-based savings

- Prioritize essential needs before wants

- Review the savings plan monthly or quarterly

This method makes the budget clearer and makes it easier to adjust when family expenses change.

7. Is a Bank Savings Deposit a Good Way to Keep Money Safe?

When should you use a savings deposit instead of keeping money in a checking account?

If you do not need to use a certain amount of money right away, placing it in savings is usually more reasonable because it keeps it separate from daily spending cash flow. A savings account is more suitable for holding money and earning interest, while a checking account mainly serves everyday transactions.

Is saving money in a bank safe?

In principle, placing money in a savings account at an institution that participates in deposit insurance is safer than holding cash. Besides protecting depositors, this option also helps you maintain discipline when you want to save money for medium-term or long-term goals.

Should you save by week, month, or longer term?

The term should depend on when you need the money, not just on the interest rate. Flexible options are more suitable for an emergency fund or short-term goals, while longer terms work better when you do not expect to use that money anytime soon.

How to choose the right savings option for your goal

If your goal is an emergency fund, you should prioritize an option that is easy to withdraw and easy to monitor. If your goal is to save money according to a plan over several months or several years, you can use this short checklist:

- Identify when you will need the money

- Prioritize flexibility if the goal is still uncertain

- Choose a longer term when you want to keep the money more stable

This makes your savings plan better aligned with your goals and easier to connect to deeper articles about how to use savings deposits effectively.

8. Common Mistakes That Make Saving Money Ineffective

Setting a goal that is too big from the start

Many people begin with strong motivation, but choose an amount that goes beyond their real ability. When the goal is too large, the savings plan easily becomes a burden and quickly causes you to lose motivation.

Trying to save without managing spending

Saving is hard to sustain if you only try to set money aside without knowing where your money is going each month. When you do not track income and your main spending categories, you can easily cut the wrong things or overlook the expenses that are slowing down your progress.

Putting all funds in one place

Another common mistake is keeping spending money, the emergency fund, and accumulated savings all together. When everything is combined in one place, it becomes harder to track progress and harder to stay disciplined with each separate goal.

Cutting too much and then giving up

Many people think that if they want to save money quickly, they must cut almost all personal spending. This may produce short-term results, but it is usually hard to sustain because it easily creates a feeling of deprivation.

Not tracking progress every month

A savings plan will be much less effective if you do not review the results each month. To avoid drifting away from your goal, you should:

- Check how much money you have actually set aside

- Compare your progress with your savings goal

- Adjust spending and savings levels when needed

Regular tracking makes the plan more realistic and reduces the risk of giving up halfway.

Conclusion

Saving money does not mean forcing yourself to live miserably or cutting out every personal need. At its core, it means intentionally keeping part of today’s income to protect personal financial stability and create room for more important plans later on.

When you have a clear goal, an approach that fits, and the discipline to stay consistent, saving becomes much more sustainable. You do not need to start with a large amount. Instead, you should start with a realistic level that you can maintain over time and gradually adjust as your situation changes.

To continue from this foundation, you can read more about ways to save money, learn how to save from your salary, or explore how to use savings deposits. If you are considering keeping your money in a bank, you should also read more about whether bank savings deposits are safe.

Frequently Asked Questions About Saving Money (FAQs)

What percentage of your income should you save each month?

There is no single ratio that works for everyone. A reasonable amount is one you can maintain consistently each month after covering essential needs, repaying debt, and keeping your budget from becoming too tight.

Should you save money if your income is low?

Yes. When your income is low, saving is not about putting aside a large amount. It is about building the habit of saving consistently, cutting expenses that are not truly necessary, and gradually creating a small but meaningful emergency cushion.

Should you keep your savings in cash or deposit them in a bank?

Cash is suitable for small amounts you may need quickly, but keeping money in a bank is usually safer and makes it easier to stay disciplined. If your goal is serious saving, setting money aside in a separate account is often more effective than keeping it in the same pool of money you use for everyday spending.

Is it more effective to save daily, weekly, or monthly?

The most effective method is the one that fits your income and spending pattern. People with a fixed salary often find it easier to save monthly, while those with irregular income may do better with a more flexible weekly approach or by saving each time they receive income.

How can you save money without feeling restricted?

Start with a small amount, set a clear goal, and cut only the expenses that are not truly necessary first. When your plan fits your current life, saving becomes easier to maintain and feels much less restrictive

References:

MoneyHelper – Managing your money

MoneySmart – Budgeting and saving

MoneySmart – Student life and money